The fundamentals of Private Equity

Access to the unlisted market

Private equity provides access tothe unlisted market, which accounts for the vast majority of companies and is often more representative of the real economy than large-cap stocks alone.

Many high-potential companies are not listed and may never be. Private equity allows investors to invest in growing companies that are in the process of being transferred, consolidated, or transformed, and which are not accessible via public markets. For investors, this means diversifying their exposure to economic drivers outside the stock market, while accepting greater liquidity constraints.

The real economy

Private equity directly finances companies: growth investments, industrial modernization, digital transformation, internationalization, sector consolidation, or shareholding transfers.

This dimension is essential: value creation comes mainly fromimproving fundamentals. It can take the form of accelerated growth, market share gains, improved margins, better management discipline, or governance restructuring. Private equity is therefore a channel for financing the real economy, with concrete impacts on the trajectory of the companies it supports.

The long term and the J curve

Private equity is an asset class that is fundamentally oriented toward the long term. A fund is generally structured for a period of eight to twelve years, with an initial investment phase, followed by a value creation phase, and finally a divestment phase.

This time lag explains the J-curve. In the early years, performance may appear weak or even negative, particularly due to setup costs, portfolio ramp-up, and the investments needed to transform companies. As value creation plans take effect and exits are realized, performance becomes more apparent.

The J-curve is therefore not an anomaly: it is a structural feature of private equity, which requires results to be evaluated over a full cycle rather than in the short term.

_1200px_under_100kb.webp)

Alignment of interests

The private equity model is based on a structured alignment between three parties: the General Partners (GPs) who manage the fund, the Limited Partners (LPs) who provide the capital, and the management teams of the companies.

This alignment is facilitated by the compensation and governance structure. On the one hand, the manager’s compensation often includes a variable component (carried interest) that depends on performance. On the other hand, the executives of the portfolio companies are frequently equity partners, which is intended to align their decisions with long-term value creation. Within a well-structured framework, private equity therefore seeks to reduce the traditional disconnect between investors and operational teams.

How does the asset class work?

Unlike stock markets, performance in private equity does not depend primarily on daily price fluctuations. It is based above all on the ability to transform a company: improving its organization, accelerating its growth, optimizing its financial structure, and preparing for a sale under favorable conditions.

This logic leads to performance that is more closely linked to economic fundamentals than to short-term fluctuations in market sentiment. It does not eliminate risk, but it changes the nature of the drivers of return.

The structural characteristics of private equity

Three elements fundamentally structure private equity.

- The first is the long-term horizon, which allows a transformation strategy to be deployed without immediate liquidity pressure.

- The second is illiquidity, which is inherent in investing in unlisted companies.

- The third is active management: investors do not simply provide capital, they also offer strategic support to management in order to strengthen the company's competitiveness in the long term.

These characteristics explain why private equity is a distinct asset class, with its own return and risk dynamics.

The role of the General Partner and investors

The management company, known as the General Partner (GP), is responsible for the entire investment cycle. It selects target companies, structures transactions, participates in governance, and drives the value creation strategy. Investors, known as Limited Partners (LP), provide capital and delegate management to the GP within a specific contractual framework.

This relationship is based on an alignment of interests, structured by the manager's remuneration and, in most cases, by their stake in the fund. The quality of reporting, transparency on risks, and investment discipline are key criteria for evaluating a team.

The investment cycle and the timing of performance

A private equity fund goes through successive phases: investment, operational development, and finally divestment. Performance can only be accurately assessed over the course of this entire cycle. The first few years may show modest or even negative returns, before value creation materializes during exits.

There is significant variation in performance between funds. The gap between the best and worst performers can be substantial, making selection particularly crucial, especially for certain vintages or market segments.

The different vehicles for investing in private equity

FPCI Professional Private Equity Fund

The FPCI a vehicle reserved for professional investors. Its legal flexibility allows for the creation of an asset allocation tailored to a diversified private equity strategy, typically over the long term.

FCPR - French venture capital fund

The FCPR is a fund that must invest at least 50% of its assets in unlisted companies. It provides exposure to private equity within a defined regulatory framework, targeting the financing of growing or transforming companies.

SCR - Venture Capital Company

SCR is a company that invests directly in unlisted SMEs. It can be used to structure a more targeted investment strategy, particularly in innovative sectors, but requires governance and monitoring adapted to sometimes complex situations.

SLP - Société de Libre Partenariat

The SLP is a structure inspired by Anglo-Saxon models, used mainly by professional investors. It offers great flexibility in terms of management and organization, and is particularly suited to private equity transactions requiring a flexible framework.

FCPI - Fonds Commun de Placement dans l'Innovation (French innovation mutual fund)

The FCPI aims to finance innovative companies, with a requirement to invest the majority of its funds in eligible companies. It is often part of a strategy to support innovation, but must be analyzed in terms of risk level and liquidity.

These different players and types of funds make up the private equity ecosystem, each providing a specific response to a variety of financing needs.

Focus on a private equity fund of funds?

What is a private equity fund of funds?

A private equity fund of funds is an investment vehicle that does not invest directly in companies, but rather in a selection of funds managed by different general partners (GPs). This structure aims to build, through a single vehicle, greater diversification than an investor would obtain by selecting a single fund.

The economic logic behind a fund of funds is based on reducing idiosyncratic risk: performance is no longer linked to a single team, strategy, or vintage, but spread across a portfolio of funds. This approach can also provide access to established teams that are sometimes difficult to access, while benefiting from a professional management framework.

The objectives of a private equity fund of funds

A fund of funds acts as a strategic intermediary, selecting and allocating capital to a variety of funds managed by different General Partners. This selection is based on an in-depth analysis of the teams, their investment discipline, their ability to create value, and the consistency of their strategy.

Risk diversification

Diversification in funds of funds can be assessed in several ways: geographical areas , sectors, but also styles (buyout, growth, venture, special situations). The aim is not to eliminate risk, but to limit the impact of an isolated underperformance on the portfolio as a whole.

Access to exclusive opportunities

Some sought-after funds are closed to new investors or require high minimum investment amounts. A fund of funds can facilitate access to these strategies while pooling due diligence monitoring efforts with specialized teams.

Maximizing long-term returns

By diversifying exposure and selecting managers capable of delivering performance over several cycles, a fund of funds aims to build a more robust return trajectory over time. However, this robustness depends on fees, the quality of selection, and consistency of allocation between vintages.

Access to private equity is mainly through closed-end funds, which generally have a lifespan of between eight and twelve years. Investors commit to contributing a certain amount of capital, which will be called down gradually as investment opportunities are identified by the management company. Investing in funds of funds involves risks, including the risk of capital loss and liquidity risk.

Private equity fund of funds management fees

Funds of funds generate costs at two levels, which distinguishes them from funds that invest directly.

Direct costs

They remunerate the management of the fund of funds itself and cover, in particular, the selection, monitoring, and administration of the vehicle. They generally include management fees, as well as operating costs (audit, legal, custodian, administration).

Indirect costs

These fees correspond to the costs incurred by the underlying funds, including their management fees and, where applicable, the carried interest . This two-tiered fee structure can weigh on net performance and must be evaluated in light of the expected benefits: diversification, access, and quality of selection.

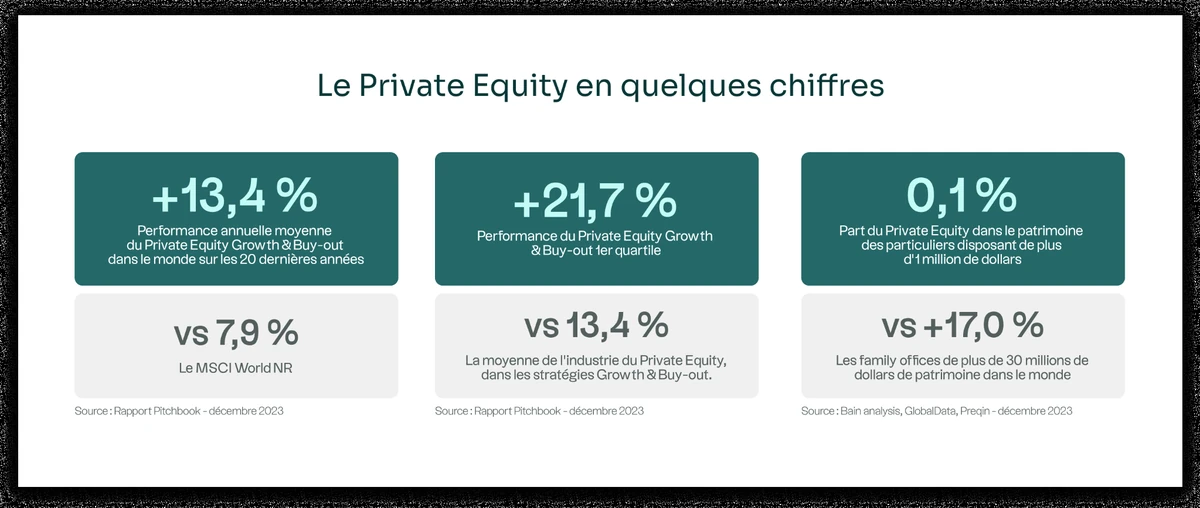

Private equity strategies: venture, growth, and buyout

Private equity encompasses several strategies corresponding to different stages of maturity of the companies financed.

Venture Capital

Venture capital finances innovative companies in the start-up or acceleration phase. Business models are often still under development and the target markets may be emerging.

Value creation comes mainly from future growth and the company's ability to reach critical mass. The risk of failure is structurally high, which means results vary a lot. In this segment, portfolio diversification is key, as a few big wins can make up for several underperforming investments.

Growth Capital

Growth Capital targets established companies with a proven business model and demonstrated or near-proven profitability. The objective is to accelerate growth, for example through international expansion, industrial investment, commercial reinforcement, or targeted acquisitions.

Value creation is based on scaling up, improving organization, and the ability to sustain controlled growth. The risk profile is generally intermediate between Venture and Buyout, with greater visibility on cash flows.

The Buyout (LBO)

A buyout, often structured as LBO, typically involves mature companies that generate recurring cash flows. The transaction combines equity and debt financing to optimize the capital structure.

Value creation depends primarily on the quality of execution: operational improvement, organic growth, acquisitions, financial discipline, and governance. Leverage can amplify the performance of equity capital, but it also increases sensitivity to the macroeconomic environment and financing conditions.

The Turnaround

Turnaround targets companies that are underperforming operationally or experiencing financial difficulties. The intervention involves implementing a structured recovery plan, which may include debt restructuring, cost rationalization, or strategic repositioning.

This segment requires in-depth expertise, as value creation depends on the ability to restore profitability and financial strength. When mastered, it can generate significant value creation, but the initial risk is higher.

_1200px_under_100kb.webp)

How can private individuals gain access to private equity?

Specialized platforms:

Some online platforms dedicated to private equity offer solutions that are more accessible to individuals. Depending on the platform, they allow users to select projects or funds based on criteria such as sector, geography, or strategy. Digitalization simplifies the subscription process, but investors must remain mindful of liquidity, fees, selection quality, and the regulatory framework.

Funds dedicated to individuals

Some management companies structure funds designed for non-professional investors, with lower entry thresholds than institutional standards. The main advantage lies in pooling and professional management. The trade-off is often limited liquidity and a fee structure that needs to be analyzed carefully.

Life insurance and structured products

Private equity can be integrated into certain life insurance contracts or wealth management packages, depending on the offering. This approach can provide a degree of operational simplicity and, in some cases, a tax framework, but it does not eliminate the risk of capital loss or the liquidity constraints inherent in unlisted investments. Transparency regarding fees and redemption terms is key.

The real drivers of value creation in private equity

Performance in private equity is not based on a single lever, but on a consistent combination of strategic, operational, and financial actions deployed over several years. This value creation is a long-term process and requires disciplined execution.

Organic growth and strategic positioning

The primary driver of value creation lies in the organic growth of the companies we support. This involves identifying sectors driven by structural trends and companies capable of gaining market share on a sustainable basis.

Improving competitive positioning, optimizing the offering, pricing strategy, and commercial efficiency help increase revenue and strengthen margins. This dynamic is a key driver of performance.

Operational support and active governance

Beyond financing, private equity relies on demanding governance and close operational support. Funds work alongside management to structure the organization, professionalize decision-making, and implement performance indicators.

This active governance aims to reduce operational blind spots and accelerate execution. Aligning interests, particularly through management share ownership, strengthens the consistency between strategic objectives and value creation.

External growth and synergies

Value creation can also come from an external growth strategy. Acquiring complementary businesses can accelerate development, broaden the offering, strengthen market position, and generate synergies.

This approach requires strong discipline in the selection of targets and, above all, in integration, which often determines industrial success.

Optimizing the financial structure

In certain strategies, particularly buyouts, controlled financial leverage can optimize the capital structure. Debt, when carefully calibrated, can improve the return on equity.

However, this leverage is only relevant if the company has resilient cash flow generation and sufficient visibility on its future cash flows. Leverage does not create value in itself: it mainly amplifies execution, either favorably or unfavorably.

Long-term investment and exit discipline

Private equity involves holding investments for several years. This long time frame allows for the implementation of a structured value creation plan, followed by preparations for an exit.

The sale, whether to an industrial buyer, another fund, or via an initial public offering, is a decisive step. Market conditions play a role, but the quality of the preparatory work, governance, and the strength of the fundamentals have a strong influence on valuation.

Performance indicators in private equity

The performance of a private equity fund is assessed using several complementary indicators.

The internal rate of return (IRR )

It measures annualized profitability by taking the time factor into account.

Multiple of invested capital (MOIC)

It indicates how many times the capital invested has been multiplied.

Other indicators exist, such as DPI, which reflects the amounts actually distributed, or TVPI, which includes the residual value of equity investments, allowing for an analysis of performance at different stages of the fund’s lifecycle.

These metrics must be interpreted over the entire investment period and viewed in the context of the macroeconomic environment, the strategy segment, and the vintage.

_1200px_under_100kb.webp)

.webp)

.webp)

.jpeg)

.webp)

.webp)

.webp)

.webp)

.webp)

.jpeg)

.webp)