What is the actual performance of private equity?

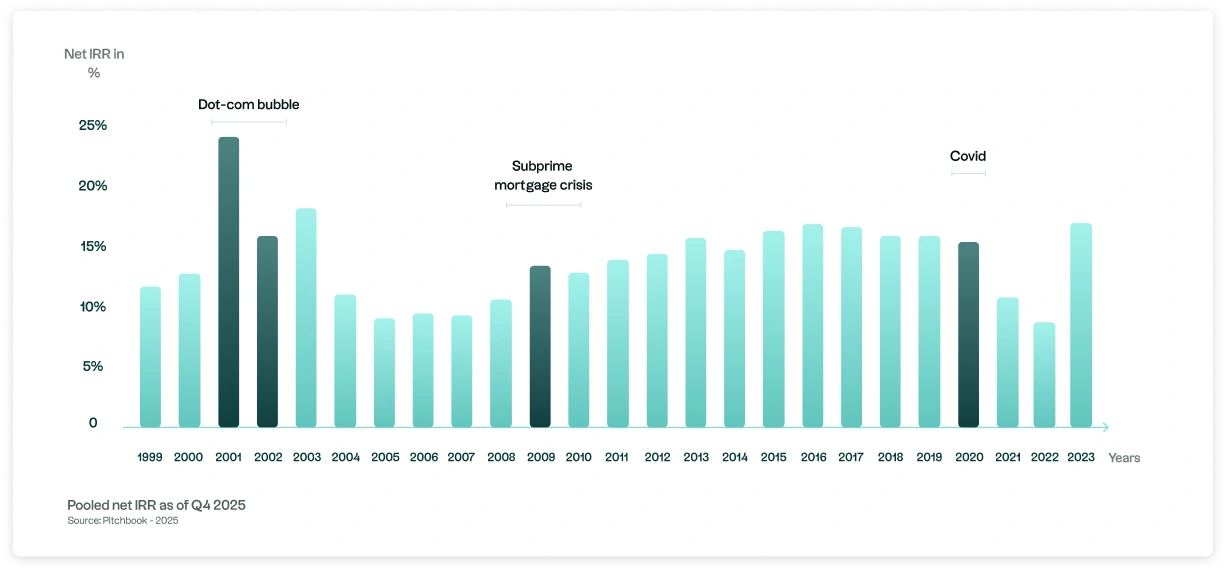

Private equity performance is best assessed over long-term cycles. Unlike public markets, where valuations fluctuate on a daily basis, private equity operates on a longer economic horizon, typically ranging from eight to twelve years.

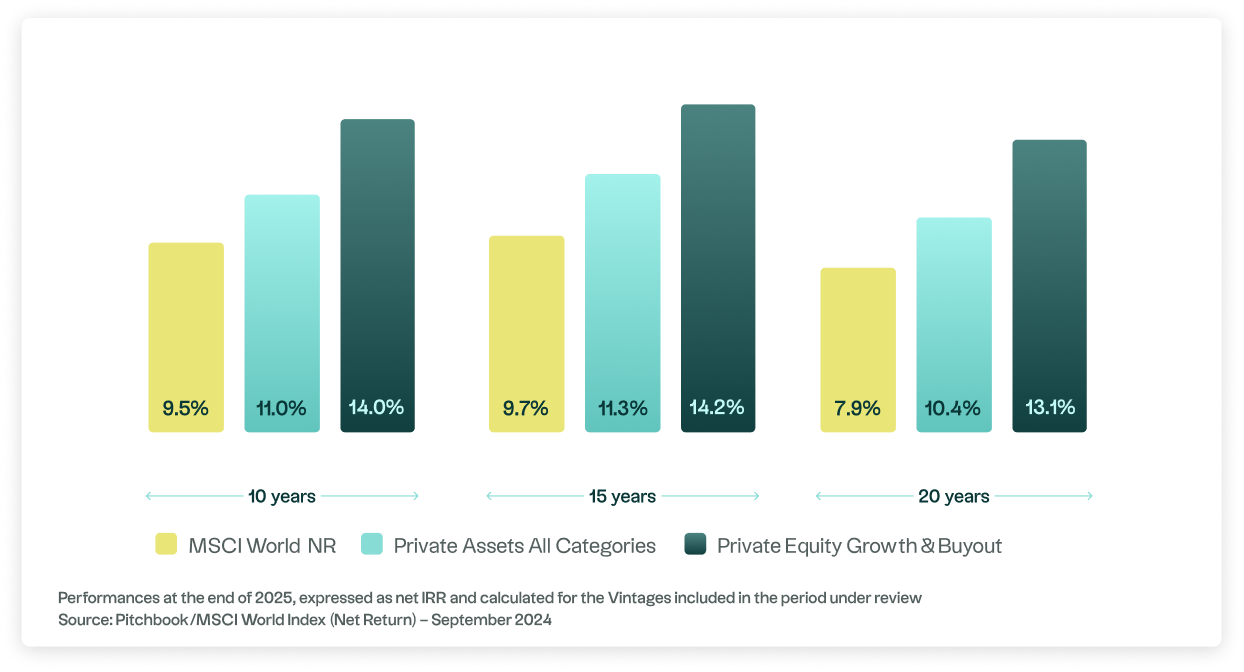

Sector data highlight historically superior performance levels for private equity, though a nuanced interpretation is warranted. Over the long term, French private equity has posted an average IRR of 13.3% per year over 20 years, according to France Invest, compared to annualized returns of around 7% to 8% for the CAC 40 over a comparable time horizon. Internationally, the McKinsey’s Global Private Markets Report 2025 also highlights the outperformance of private equity relative to U.S. equity markets since the early 2000s.

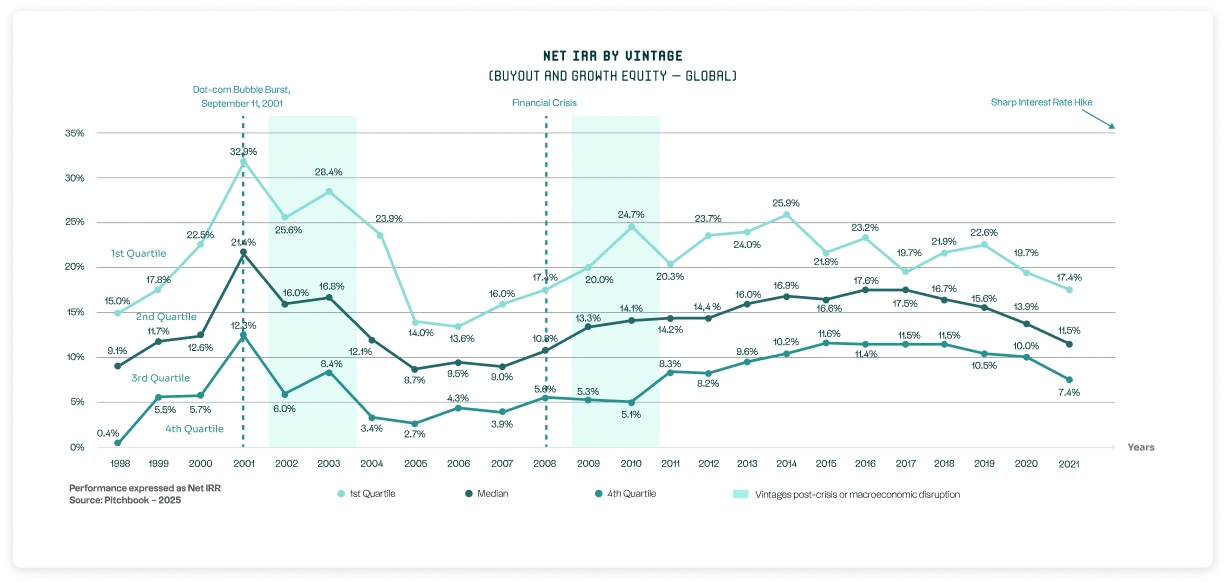

However, this trend is accompanied by significant variation in performance across funds and investment rounds. According to Preqin and Cambridge Associates, buyout funds in the top quartile have historically generated IRR ranging from 15% to 25% depending on the period, illustrating the critical role of management team selection.

These data, derived from historical analyses, are not indicative of future performance and should be evaluated in light of the specific characteristics of private equity, particularly its long investment horizon and structural illiquidity.

The internal rate of return ( IRR) is the benchmark metric. It measures annualized returns by taking into account all cash flows. In addition, an analysis of the return on invested capital is used to assess absolute value creation. These metrics should always be interpreted with caution, as they vary significantly depending on the year and the fund manager.

Private equity performance should never be analyzed in isolation. It only makes sense when it is part of a coherent long-term asset allocation strategy.

Why can private equity generate superior returns?

Private equity performance is driven primarily by two structural mechanisms:

The first is the illiquidity premium. By agreeing to tie up their capital for a long period without the possibility of immediate withdrawal, investors demand additional compensation. This illiquidity constraint is a central component of the expected return.

The second driver is the creation of operational value. Private equity firms play a direct role in corporate governance, strategy, and financial structuring. They work closely with management to optimize margins, pursue external growth, and expand into international markets. This active involvement is what fundamentally distinguishes private equity from public markets, where investors remain passive.

It is important to note, however, that no returns are guaranteed. There is a significant gap in performance between the top-performing funds and the worst-performing ones. Investment selection expertise therefore plays a decisive role.

What are the risks associated with private equity?

Analyzing the risks of private equity requires a clear-headed and structured approach. This asset class involves specific risks that differ from those of public markets.

The first risk is illiquidity. A private equity investment involves a commitment spanning several years. Investors generally cannot recover their capital until the holdings are gradually liquidated. This constraint requires careful financial planning and an asset allocation strategy tailored to the investor’s overall liquidity profile.

The second risk is the risk of capital loss. Portfolio companies may encounter operational difficulties, face an industry downturn, or be affected by an unfavorable macroeconomic environment. Like any equity investment, private equity exposes investors to the risk of losing some or all of their investment.

The third risk relates to fund selection. Private equity performance depends heavily on the quality of Fund manager, their sector expertise, their investment discipline, and their ability to support management teams. The performance gap between the top and bottom quartiles can be significant. This variation poses a risk in itself for investors who are insufficiently diversified or poorly advised.

Finally, the economic environment directly influences acquisition, financing, and exit terms. Rising interest rates or an economic slowdown can weigh on valuations and extend holding periods.

How can one analyze the risk-return profile of private equity?

The risk-return profile of private equity cannot be fully understood without taking the time dimension into account. The early years of a fund are often characterized by outflows related to investments and expenses. Value creation then gradually takes shape before materializing upon exits. This phenomenon is known as the J-curve.

A long-term perspective is therefore essential. An investor constrained by a need for short-term liquidity will not be able to cope with the very nature of this asset class.

Diversification also plays a key role. Diversifying by vintage helps smooth out exposure to economic cycles. Diversifying by strategy and geographic region reduces reliance on a single market segment. This systematic approach is the one adopted by the majority of institutional investors.

Finally, a disciplined selection process remains crucial. A thorough analysis of track records, team stability, and alignment of interests is essential for managing risk.

Is private equity riskier than the stock market?

Private equity is often compared to public markets, but this comparison requires a nuanced understanding of risk profiles. Private equity appears to be less volatile because valuations are not determined on a daily basis, which contributes to greater portfolio stability over time. This characteristic does not reduce the underlying economic risk, but it does alter perceptions of that risk and its timing.

Furthermore, while illiquidity and performance variation among managers are higher than in public markets, private equity stands out for its ability to intervene directly in companies. This approach makes it possible to leverage operational value creation drivers that are less dependent on short-term market conditions.

Thus, rather than simply representing a contrast in terms of risk level, private equity is characterized by a distinct profile that, under certain conditions, can offer greater control over the drivers of long-term performance.

For which investors is private equity a suitable option?

Private equity is primarily aimed at investors with a long-term investment horizon and the ability to tie up a portion of their capital. It is particularly well-suited to structured portfolios seeking diversification beyond listed equities and bonds.

However, it is generally not suitable for investors with a low risk tolerance or a need for quick liquidity. The overall consistency of the asset allocation remains the key factor.

Private Equity: Risks and Returns

Is private equity performance guaranteed?

No. Private equity involves the risk of capital loss, and performance varies significantly depending on the fund and economic cycles.

Why does the performance seem less volatile?

Because valuations are conducted periodically, not daily. Economic volatility exists, but it is not continuously monitored as it is in publicly traded markets.

Is illiquidity merely a risk?

It poses a major challenge, but it is also a potential source of additional returns.

Can private equity be included in a traditional asset allocation strategy?

Yes, provided that the overall portfolio remains consistent, is sufficiently diversified, and has an appropriate investment horizon.

.webp)

.webp)