What is unlisted investment?

Summary definition

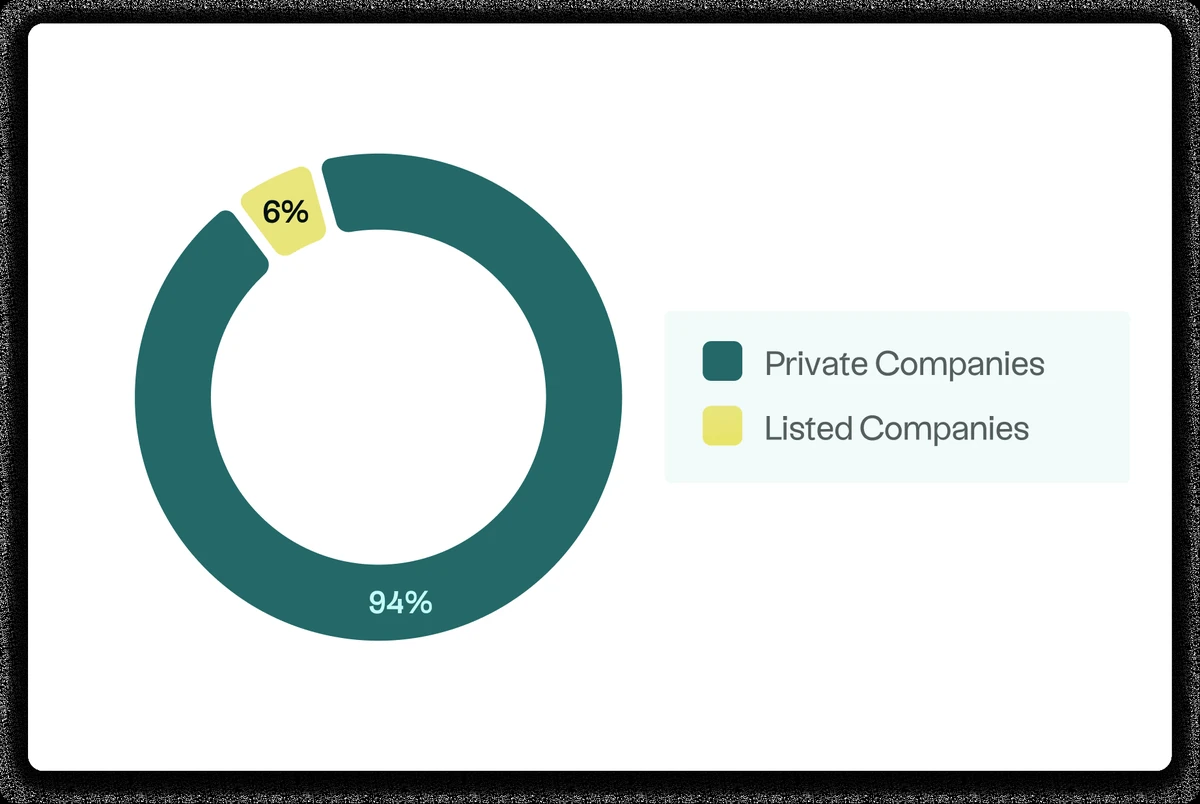

Unlisted investments include all investments made outside the stock markets. They can involve private companies as well as unlisted real estate assets, private debt, infrastructure, and even innovation and disruptive technology projects, particularly in deep tech.

These investments are not subject to daily trading. They are characterized by less frequent valuation, often long-term horizons, and exposure to operational dynamics rather than instantaneous market movements.

Why do some companies remain unlisted?

Many companies voluntarily choose to remain private for several structural reasons. Some prefer to have greater control over their capital, which allows them to maintain tight governance and limit dilution.

Others are seeking a reduction in regulatory obligations and disclosure requirements imposed on listed companies, in order to devote more time to operational development.

This choice is also explained by the desire to implement strategic plans over several years, without being subject to the pressure of quarterly results. Finally, some companies prefer to rely on specialized investors who can provide operational support rather than resorting to market financing.

The main categories of unlisted investments

The private markets universe comprises several segments:

- Private Equity: venture capital, growth equity, buyout financing (LBO).

- Unlisted real estate.

- Private debt.

- Infrastructure.

Each category has its own risk profile, valuation dynamics, and horizon.

Why is interest in unlisted companies growing in 2026?

A historically institutional asset class

The growing interest in unlisted securities in 2026 is part of a trend that is already well established among institutional investors. Insurers, pension funds, and sovereign wealth funds have been using them for several decades to supplement their portfolios with assets that are less dependent on stock market fluctuations.

Their objective is to strengthen long-term visibility, smooth out the impact of economic cycles, and contribute to the financing of the real economy. This also provides direct support for the growth of unlisted companies.

This institutional practice, now better documented and more widely understood, helps to legitimize the appeal of unlisted companies to a broader audience.

Specific value creation drivers

The unlisted market relies on value creation drivers that differ significantly from those observed on public markets.

- Structured and active governance, enabling managers to intervene more directly in the strategic direction of companies. This proximity facilitates operational monitoring, rapid decision-making, and alignment between shareholders and executives.

- Operational initiatives designed to improve performance in the long term, such as process optimization, team strengthening, investment in digitalization, or opening up new markets. These actions are generally part of multi-year plans, with gradual implementation.

- Strategies developed over several years, enabling us to support companies through profound transformations. This long-term approach allows us to carry out structural projects, which are often difficult to implement in a listed environment subject to strong short-term pressure.

These mechanisms are often observed in the unlisted market, but they do not guarantee results or eliminate the associated risks.

The role of diversification

Diversification is one of the most frequently cited reasons for the growing interest in private markets in 2026.

- Expanding the diversity of the portfolio companies, thanks to access to companies of various sizes, maturities, and sectors, which are often absent from public markets. This variety makes it possible to integrate growth drivers that differ from those available inthe listed universe.

- Exposure to a variety of sectors and geographic areas, which can help balance a portfolio, particularly when economic cycles are not synchronized across regions or sectors.

- Less sensitivity to daily market fluctuations, as valuations of unlisted companies change less frequently and are more closely linked to operational performance than to market sentiment. This characteristic can mitigate perceived volatility, even if it does not eliminate underlying economic risks.

Together, these factors explain why unlisted securities continue to attract increased interest in 2026. This is a context in which investors are seeking to strengthen long-term diversification and access sources of value creation that differ from those offered by public markets.

This diversification remains theoretical and does not prejudge future performance.

Private equity: a key pillar of private markets

Within private markets, private equity occupies a special place. This is due to its economic weight, the diversity of its strategies, and its role in financing companies. It is often the main entry point into the private market for both institutional and sophisticated investors.

Rather than forming a homogeneous block, private equity encompasses several distinct approaches. Each reflects the diversity of the economic fabric being financed.

Some strategies focus on young, innovative companies that are still in the process of establishing themselves. Others target more established companies with a proven operational and financial track record.

This diversity allows a portfolio to be exposed to a variety of value drivers, linked sometimes to innovation, sometimes to organic growth, and sometimes to the optimization of existing models.

In a long-term allocation, private equity is thus viewed as a set of complementary sub-strategies, each with specific risk, time horizon, and value creation profiles.

How is a private equity investment organized in practical terms?

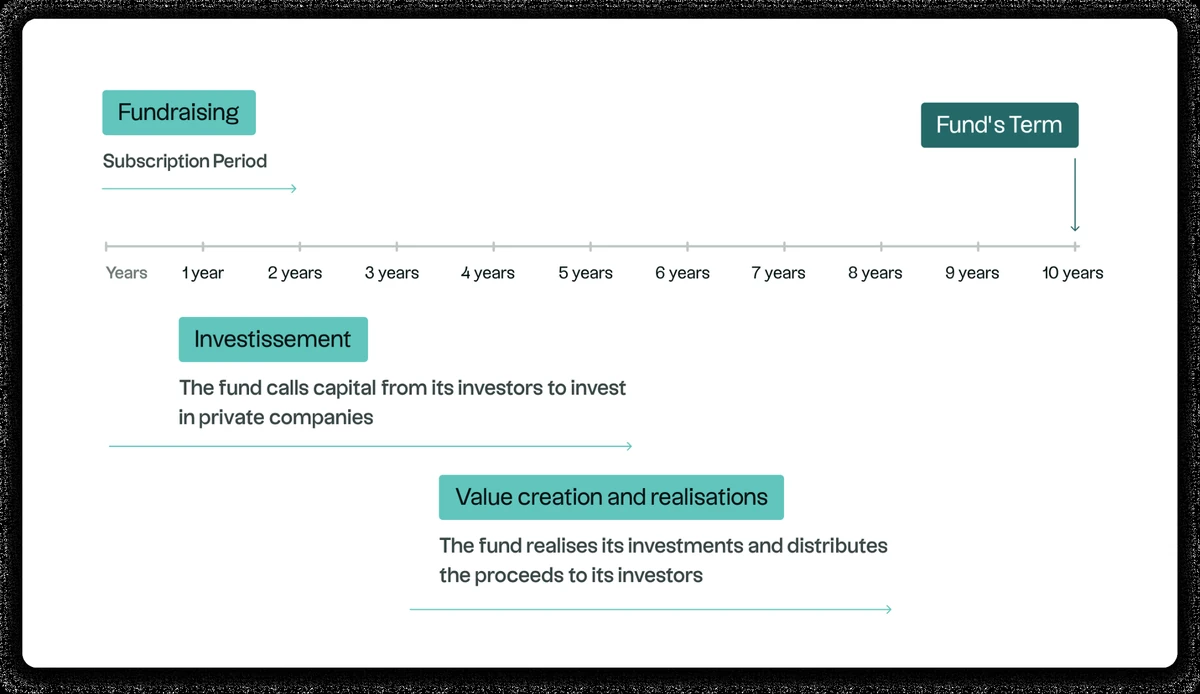

Investing in private equity involves committing to a structured time frame, which is very different from listed investments.

The commitment is generally made within a collective vehicle, whose capital is deployed gradually.

After the fund has been set up, the capital committed is called up over several years to finance successive investments.

This period is followed by a phase of support for companies, during which management teams implement their development, optimization, or transformation plans. Exits, meanwhile, take place in stages, depending on market opportunities and the maturity of the investments.

This approach implies limited visibility in the short term, but is part of a long-term strategy in which value is created gradually. The overall exposure period, often close to ten years, reflects the illiquid nature of private equity and the time required to implement operational strategies.

The total duration often ranges between 8 and 12 years, reflecting the inherent illiquidity of this asset class.

.webp)

%20(1).webp)

_11zon.webp)

.jpeg)

.jpeg)