Damien Hélène, editor-in-chief ofAltaroc :

To what extent does a pension fund like PSERS use private equity to finance pensions?

Darren Foreman, former Director of Private Equity for PSERS:

There are a thousand times more private companies than public ones. So you want this asset class to be part of your portfolio allocation diversification, whether you're a pension plan or a high-net-worth investor.

At the end of the 1990s, our CIO (Chief Investment Officer) told us: "We need to increase our exposure to private equity in order to generate performance". Like many investors and public pension plans, we turned to private equity for its returns, which, over a long period of time, are better than what you can get on the stock markets.

As a result, we have considerably increased our exposure to private equity, notably by investing in the British fund Bridgepoint from the outset, and in the French PAI, in which we participated in the first fund.

D.H.: Why is private equity so attractive to pension funds?

D. F.: With private equity, you can expect to achieve better returns than with listed markets or even mutual funds, on average 300 basis points higher. The current outlook for private equity is around 10% - 12% on a net basis.

If your pension fund has a target return of 7% and you can achieve 10% in private equity, or even a little more, your returns are there. You're meeting your growth targets, which benefits your portfolio and your capital, and therefore your fund's ability to pay its bills and its beneficiaries' pensions.

D.H. : How has private equity's share of PSERS' total assets changed over the past 20 years?

D. F.: At our peak, in the early 2000s, we were committing $3 billion a year to reach 17% of our portfolio. As we were among the first to invest in private equity on a large scale, our development was very rapid, more so than we had anticipated. As a result, the proportion allocated to private equity has risen to 21%.

Since then, this share has fallen back. In 2007 and 2008, we were faced with the financial crisis. The Board of Directors then decided to reduce our targets to achieve better asset diversification, because you can never predict which year will be the right one for which asset class. So we refocused our investments to diversify.

For 2021, the Board of Directors has decided to diversify even further, and has set Private Equity targets at 12% of the investment plan. At last count, this had risen to 16% of assets under management.

D.H.: What percentage of US pension funds' assets are allocated to private equity?

D. F.: On average, across the United States, I'd say that the funds allocated annually to private equity represent 12% to 14% of portfolios. At least, that's their goal. If you look at university funds, endowments and foundations, the figure rises to 30%-40%. It all depends on the system and the project.

D.H.: Which private equity strategy - venture, growth, buyout or turnaround - was PSERS most inclined towards?

D. F.: During my 22 years at PSERS, we invested mainly in buyout, devoting almost two-thirds of our portfolio to them. We sensed that it offered greater consistency than private equity. However, there are always elements of risk. Nothing is risk-free when you invest in the financial markets.

We then turned to growth equity, which offers a better return on investment and reduces the need for financial leverage. Then we had a small percentage in venture capital, perhaps 10%. And finally, legacy secondary funds, which we mainly had in the early 2000s.

D.H.: What geographical areas does PSERS target?

D. F. : Being based in Pennsylvania in the United States, we had access to all the American private equity funds! When I worked there, we also put a lot of money into Europe, mainly Western Europe. Our investments were split 60% in the US and 40% in foreign markets, mostly in Europe with General Partners (GPs) like Bridgepoint or PAI.

D.H.: What sectors of the economy are you most profitable in?

D. F.: The technology and software sectors represented the best returns on investment because they are fast-growing businesses. Software makes high margins and profits. We invested there through funds like Hg and Insight Partners, but also other firms like Bridgepoint. Next came business services. After that, the industrial sector, healthcare and consumer goods.

In brief

Darren Foreman's career

Retired since last year, Darren Foreman worked for PSERS from 2002 to 2024, exclusively on Private Equity. After starting out as an analyst, he became a portfolio manager, then moved to senior management before becoming Director of Private Equity at PSERS. In his final years, he managed a team of four and co-chaired the fund's application committee, a form of investment committee, alongside James Del Gaudio.

Business ID card

PSERS: private equity pioneer since 1985

Founded in 1917, the Pennsylvania Public School Employees Retirement System (PSERS) is one of the oldest pension funds in the United States. It provides retirement benefits for public school employees in 763 schools in the state of Pennsylvania.

PSERS manages over $75 billion in assets, providing coverage for 256,000 active employees and 254,000 retirees. In 2024, a total of $7.7 billion was paid out to beneficiaries, for an annual average of $26,392 per annuitant 23.

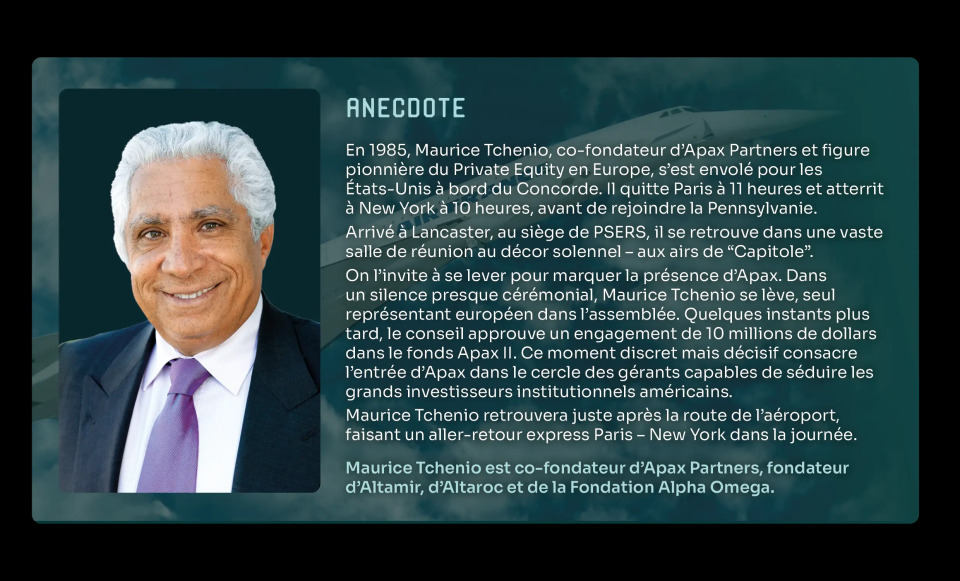

PSERS' first investment in a venture capital fund dates back to 1985, marking an early commitment to non-listed assets. On a net asset value (NAV) basis, its private equity portfolio is worth over $12 billion.

23 https://www.pa.gov/content/dam/copapwp-pagov/en/psers/documents/transparency/financial-reports/acfr/psers%20acfr%20fy2024.pdf