%2520(1).webp)

Analysis by Louis Flamand, Chief Investment Officer of Altaroc on the Private Equity environment in the first quarter of 2025

Sources: Pathway Capital 1Q25 Environment Report, Mergermarket, Pitchbook Data

A global protectionist shock

The Trump administration's announcement of new tariffs on all US imports (10% on average, and up to 145% on certain imports from China) triggered a sharp correction in the financial markets. In four days, nearly $10 trillion in global market capitalization evaporated. The IMF has revised its growth forecasts for 2025 downward: 1.8% for the United States and 2.8% for the world.

Faced with this shock, central banks have adopted a more accommodative stance, initiating gradual monetary easing amid declining inflation. The dollar has lost more than 9% since the beginning of the year. However, the impact of these measures on short-term investment remains uncertain, due to a volatile political and economic climate.

Relative resilience of private equity

Despite this instability, the private equity industry is showing resilience, notably thanks to its low direct exposure to sectors most sensitive to imports. Service-oriented companies represent approximately 50% of the value of private equity portfolios, almost double their exposure in the S&P 500. Since the pandemic, many GPs have also diversified their supply chains. Many GPs have begun to implement operational optimization strategies (pricing power, supplier contracting, partial reshoring).

The increased selectivity of the market is reflected in the 21% decrease in the number of private equity fund transactions compared to Q1 2024 (2,210 deals in Q1 2025). The total value of disposals, however, increased thanks to two exceptional transactions: the sale of Wizpar by several funds (including Insight Venture Partners) to Google ($32 billion) and that of Worldpay by the North American fund GTCR to Global Payments ($24.3 billion) - two quality assets that found buyers among strategic buyers. Thus, the cumulative value of exits via M&A reached $205 billion, its highest level since 2022.

United States: Tempered Momentum

The US buyout market recorded robust activity in Q1 2025, with $82.9 billion in investments, a 36% increase compared to Q1 2024, according to LSEG Data & Analytics. This performance, however, masks growing fragility, with an 11% drop in the number of transactions (61 deals vs. 83 in Q1 2024), and a strong refocusing on large-scale transactions: 87% of the total value for the quarter came from large-cap deals, the highest percentage since 2007.

Take-private transactions remained strong: four of the ten largest deals of the quarter were delistings, including Sycamore Partners' $23.7 billion acquisition of Walgreens, which alone accounted for nearly 30% of the total value.

Valuation multiples remain strong: the average acquisition price stands at 11.7x EBITDA, up from 10.9x in 2024 (Source: Pitchbook LCD). Financing remains stable with median leverage at 5.2x EBITDA and a slightly lower equity contribution (46.3%, compared to 48.2% in 2024).

The healthcare sector dominates (29% of the total value), followed by technology (26%), industrial services (23%), and media/entertainment (8%). Consumer and financial services, traditionally exposed to imports, each represent only 1% of volumes - a historically low level.

In terms of exits, the United States is home to some of the largest operations of the beginning of the year, including the sales of Wiz and Worldpay mentioned in the previous paragraph.

Private equity funds still have more than $1 trillion in uninvested capital ("dry powder"), including $250 billion held by funds that are already past their third year of life. This capital must automatically be invested within a relatively short time horizon (generally within 2 to 3 years), otherwise the net returns of the funds for investors (LPs) will be penalized, as they continue to pay management fees. This time pressure helps maintain investment momentum, even in uncertain times.

Major buyout deals announced in the United States in Q1 2025:

.png)

Major buyout exits announced in the United States in Q1 2025:

.png)

Europe: a brutal adjustment

The European buyout market experienced a sharp contraction in Q1 2025, with a 38% drop in value compared to the previous quarter (€26.7 billion), which had been particularly active. This decline is 19% compared to the five-year quarterly average (€32.9 billion). The mid-market segment is particularly affected: it represents only 16% of the quarter's volumes, the third lowest share since 2007.

The DACH region (Germany, Austria, Switzerland) was the most active on the continent, accounting for 41% of activity—an exceptional level, close to historical records. European high-yield credit remains accessible, with €20.7 billion of issuance in Q1, although spreads tightened at the end of the quarter (with spreads on BB-rated bonds rising from March).

Among the key transactions: the carve-out of Sanofi's consumer healthcare division (Opella Healthcare) by CD&R for €8.0 billion, the acquisition of Apleona for €4.0 billion by Bain, and the takeover of Viridium (€3.5 billion).

Main buyout deals announced in Europe in Q1 2025:

.png)

Main buyout exits announced in Europe in Q1 2025:

Asia: general decline

The Asian market saw a 70% drop in deal value compared to Q4 2024, to $14.0 billion, with only 908 transactions (-46% year-on-year). This decline is mainly due to the absence of large-cap transactions, in sharp contrast to the recovery observed in 2024. Japan is holding up, with two notable carve-outs led by Bain. India is doing well with a 21% increase in the number of transactions, even if volumes (total transaction value) are down slightly. Conversely, China remains mired in a prolonged slump.

IPOs on the continent are also down, with 171 introductions for only $8.6 billion raised (–49% compared to the previous quarter).

Main buyout deals announced in Asia in Q1 2025:

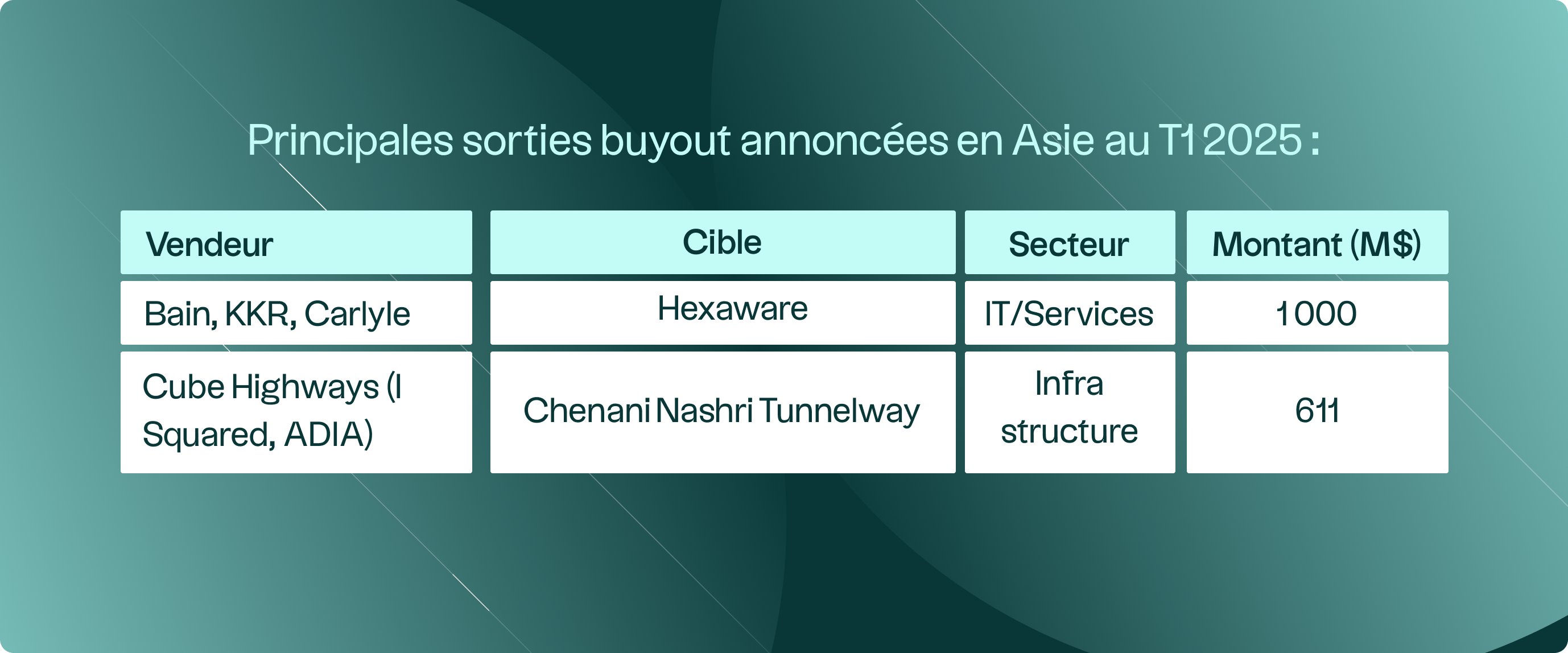

Major buyout exits announced in Asia in Q1 2025:

IPOs and the secondary market

Initial public offering (IPO) markets also remained subdued during the quarter, hampered by declining valuations in listed equity markets and increased volatility. Only eight private equity-backed companies went public in the United States during the quarter, raising $4.3 billion, in line with the quarterly average for 2024. However, the quarter saw two notable deals: the $1.5 billion IPO of CoreWeave (cloud infrastructure) in late March, and the $1.4 billion IPO of SailPoint Technologies (cybersecurity, backed by ThomaBravo) in mid-February.

Consistent with broader public market trends, the post-IPO performance of new private equity-backed companies deteriorated at the end of the quarter, with an average return of –4% between IPO and quarter-end. Many planned deals were postponed in April. Increased volatility, particularly related to trade tensions and tariffs, is weighing heavily on hopes of a recovery in the US IPO market in 2025. Several planned IPOs, including those of flagship companies like Klarna and StubHub, have been postponed pending a return to sufficient stability.

At the same time, so-called "GP-led" transactions continue to grow as an alternative to traditional exits. They allow a fund manager ("General Partner" or "GP") to extend the holding of one or more assets by transferring them to a new fund, called a "continuation fund." Investors in the initial fund can then choose to either recover their money immediately or remain invested in the new structure. This type of transaction now represents nearly half of the secondary market and is establishing itself as a key tool for actively managing portfolios in a context of more complex exits.

Continued pressure on distributions and persistent volatility in listed markets are increasing the appeal of these structures, both for GPs seeking additional time to maximize value creation, and for LPs who see them as a partial source of liquidity.

The trend is expected to continue in 2025, with an increasing number of GPs using this mechanism to extend the holding of their best assets in an environment where traditional exit options remain limited.

Fundraising: Extreme Concentration and Market Polarization

Buyout fundraising fell 41% in Q1 2025 to $34.9 billion, its lowest level since late 2015. This is primarily due to the lack of very large fund closings this quarter. This situation is expected to reverse in the coming months: several major players such as KKR, Thoma Bravo, and Clearlake are in the advanced stages of fundraising, with targets between $15 billion and $24 billion per fund. Once closed, these vehicles could significantly reactivate overall fundraising volume.

The outlook for the fundraising market in 2025 will likely depend on a sustained recovery in the M&A market, which could alleviate the liquidity crisis facing some institutional investors and encourage managers to return to the market with new vehicles. The combination of a decline in listed equity markets and a reduced level of distributions could, however, generate "denominator effect" constraints for some LPs, further increasing competition in an already tense fundraising environment. Indeed, the "denominator effect" is a phenomenon that can slow new commitments from institutional investors: when the share of unlisted assets (such as Private Equity) mechanically increases in a portfolio due to a decline in listed markets, these institutions must temporarily slow their new commitments to meet their target allocations.

Conclusion

The first quarter of 2025 was marked by a resurgence of geopolitical risks and high market volatility. In this uncertain environment, very high-quality assets, in defensive sectors such as Software and Healthcare, continue to attract sustained interest from investors. For managers capable of building such high-quality assets, exits continue to be fluid, with consistent and growing interest from industrial players.

It's also important to remember that private equity is inherently a long-term investment strategy. As the past two decades, marked by major crises—2001, 2008, 2020—have demonstrated, the industry has always been able to bounce back, adapt its models, seize countercyclical opportunities, and generate value. The current blockages in primary markets, slow fundraising, or slow exits are not unprecedented: they are organic mechanisms that naturally regulate the excesses of certain phases of the cycle. In the medium term, these conditions can create a favorable entry point: valuations normalize, competition for deals diminishes, and quality managers continue to operate within an active, disciplined, and opportunistic framework. The private equity industry has repeatedly shown that it can transform periods of tension into drivers of future performance.

.png)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

_11zon.webp)