It's no secret that the pay-as-you-go pension system is coming under increasing pressure as the population ages and contributions stagnate. While discussions between the government and social partners on a possible reform remain without a clear outcome, Altaroc puts forward capitalization as a credible, indeed indispensable, complement to ensure a decent income for future retirees.

Two scenarios, based on simple assumptions and investment vehicles already available on the market, illustrate the power of compound interest over a long period. These projections assume that a fraction of current contributions or voluntary payments is allocated to long-term investments in assets such as private equity, with a net annual return of 9%.

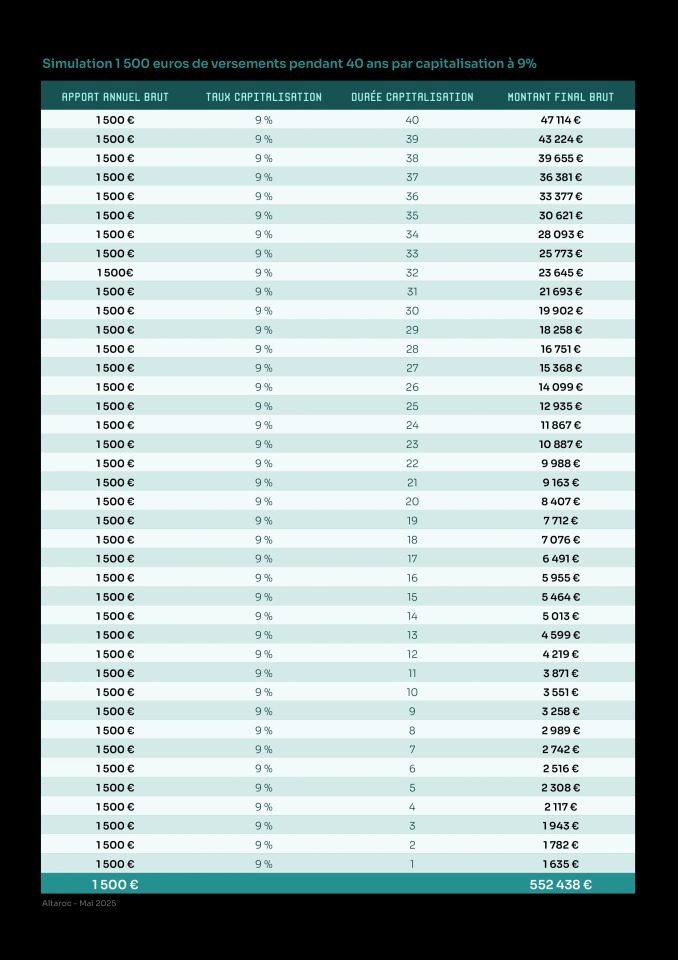

In the first case, a 25-year-old employee earning €30,000 gross a year would see his employer allocate €1,000 a year to a capitalization plan, topped up with €500 in annual personal savings. Over 40 years, this cumulative effort of €60,000 would produce a final capital of over €550,000. On retirement, this amount could be withdrawn all at once, or generate an annual income of almost €50,000, while preserving the initial capital.

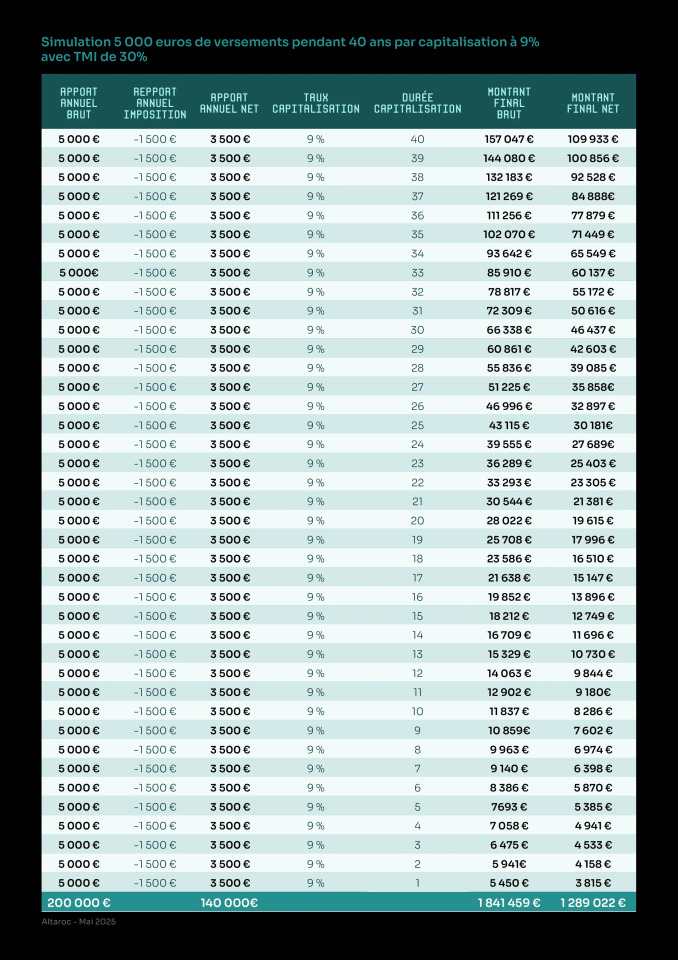

The second, more ambitious scenario assumes that a higher-paid employee (€80,000 a year) contributes €5,000 a year to a Pension Savings Plan (PER). Benefiting from a tax advantage linked to his marginal tax rate, his net effort is limited to €3,500 per year. The result: at the end of 40 years, the net capital after tax would be close to €1.3 million. This would generate a gross life annuity income of over €160,000 a year.

These spectacular figures reflect less a commercial promise than a mathematical reality: that of compound interest, for which discipline and duration are the keys. They also underline the need to educate regulators and savers alike, as compounding is still perceived as a political taboo in France.

For the time being, no regulatory provisions are needed to generalize these practices to those who can afford them. But extending the model - by allocating a portion of employer contributions to individual plans - would require agreement between social partners and public authorities. A prospect which, in the current social context, is likely to meet with strong resistance.

But beyond the individual stakes, this is also a collective opportunity: by enriching the French, private equity could also enrich France. By channelling a portion of long-term savings into funds that finance innovative, growing companies, this capital would feed directly into the real economy, supporting employment, competitiveness and tax revenues. The virtuous circle is obvious: citizens with stronger assets become more solid consumers and investors, while better-capitalized companies accelerate their expansion. In a country that is often reluctant to capitalize, it is important to remember that individual prosperity and national wealth are not antagonistic - they are intimately linked.

.jpeg)