Private Equity performance and risks

Learn about the performance and risks of this asset class

Asset class risks

The risks of Private Equity

performance history

Private Equity's historic performance

Historical performance of Private Equity funds

The overall performance of French Private Equity measured over 15 years averages 12.2%* per annum, net of fees and carried interest. It outperformed other major asset classes, notably the CAC 40 (5.1%*) and real estate (6.3%*). The asset class also outperforms globally, with an average of +16.41%** over 10 years.

Historical performance of top quartile funds

Private Equity funds are ranked in order of performance. The top quartile corresponds to the top 25% of funds. In France, first-quartile funds have achieved an average annual IRR of 25.7%* since inception. Globally, top-quartile performance has fluctuated between 14% and 31%** per Vintage over the past 25 years.

* Source: France Invest / EY (Performance Study 2021)

** Source: Pitchbook September 2023

Private Equity investment involves risks of liquidity and capital loss. Past performance is no guarantee of future results.

* Source: France Invest / EY (Performance Study 2021)

** Source: Pitchbook September 2023

Private Equity investment involves risks of liquidity and capital loss. Past performance is no guarantee of future results.

The 4 Private Equity segments

Value creation

Private Equityvalue creation levers

Private Equity applies timeless recipes for value creation.

Performance

Measuring Private Equity performance

The performance of Private Equity funds is appreciated over the long term.

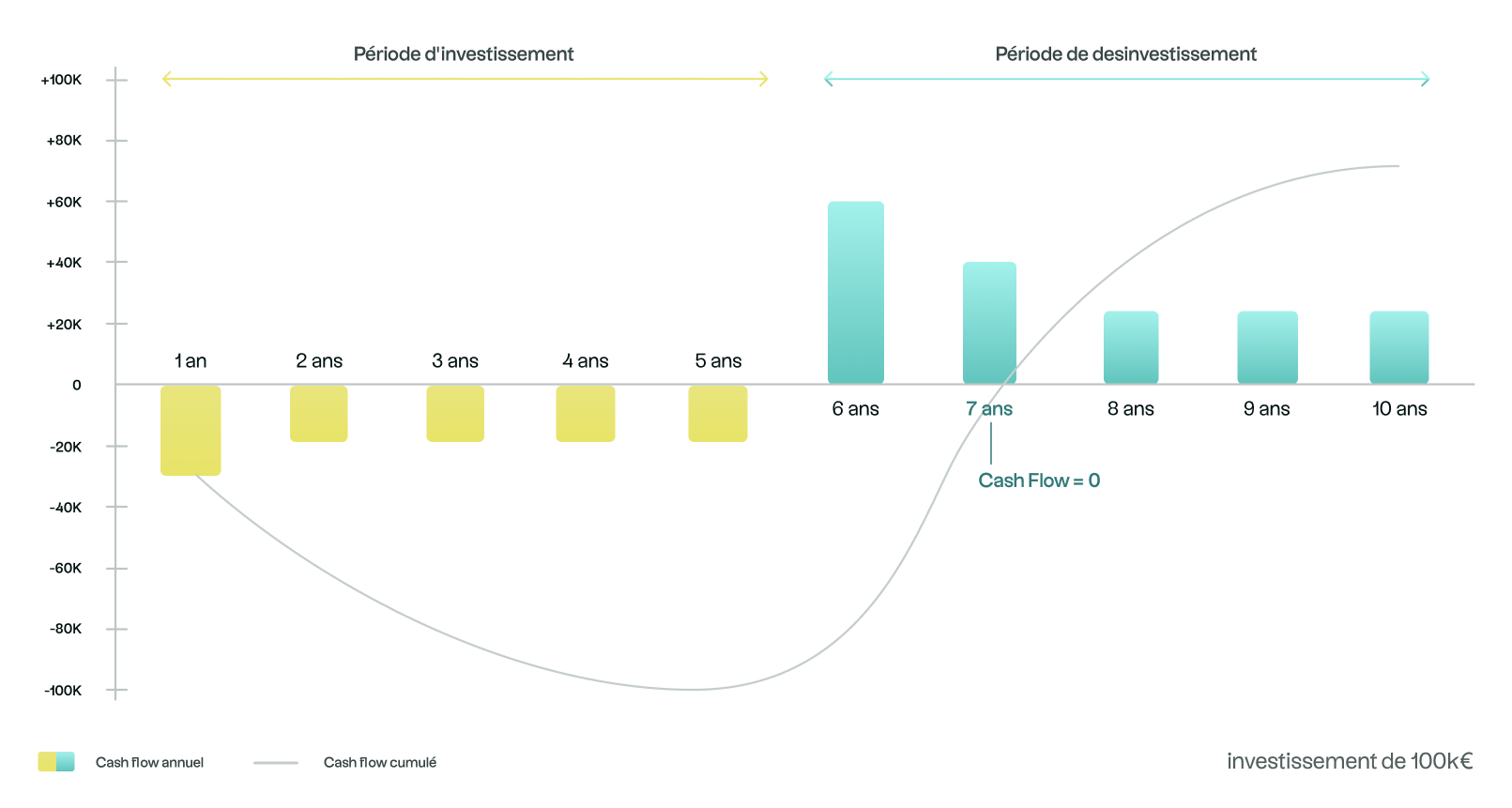

The fund traditionally deploys its capital over a period of 5 years, and the traditional holding period is also around 5 years for each holding.

Assuming that the fund realizes on average 2X its stake on each investment, it will generally return all the funds committed by its subscribers from the 7th year onwards.

Investors will therefore realize capital gains on their investments from year 8 onwards.

As fund units are not listed on a liquid market, investors cannot measure the profitability of their investment by the evolution of a stock market price.

The performance of a Private Equity investment is measured in terms of multiple of capital invested (MCI) and internal rate of return (IRR).

Assuming that the fund realizes on average 2X its stake on each investment, it will generally return all the funds committed by its subscribers from the 7th year onwards.

Investors will therefore realize capital gains on their investments from year 8 onwards.

As fund units are not listed on a liquid market, investors cannot measure the profitability of their investment by the evolution of a stock market price.

The performance of a Private Equity investment is measured in terms of multiple of capital invested (MCI) and internal rate of return (IRR).

The life of a Private Equity fund

Performance

TVPI or fund multiple

Le TVPI, ou Total Value Paid In, se calcule ainsi :

TVPI = (Distributions versées + valeur estimée du portefeuille) / Montant total appelé.

Il se décompose en : TVPI = DPI + RVPI

Paid In : montant appelé auprès des investisseurs

DPI (Distribution to Paid In) : Montant distribué aux investisseurs rapporté à leurs investissements dans le fonds

RVPI (Residual Value to Paid In) : Juste valeur du fonds rapporté aux montants investis

TVPI > 1 :

La somme de la valeur du portefeuille et des distributions réalisées est supérieure au capital investi ; le fonds est donc en position de gain en capital.

TVPI < 1 :

Le fonds n’a pas encore créé de valeur.

TVPI = (Distributions versées + valeur estimée du portefeuille) / Montant total appelé.

Il se décompose en : TVPI = DPI + RVPI

Paid In : montant appelé auprès des investisseurs

DPI (Distribution to Paid In) : Montant distribué aux investisseurs rapporté à leurs investissements dans le fonds

RVPI (Residual Value to Paid In) : Juste valeur du fonds rapporté aux montants investis

TVPI > 1 :

La somme de la valeur du portefeuille et des distributions réalisées est supérieure au capital investi ; le fonds est donc en position de gain en capital.

TVPI < 1 :

Le fonds n’a pas encore créé de valeur.

TVPI rises reflecting the value creation achieved with the passage of time.

Investment in Private Equity involves risks of liquidity and capital loss. Past performance is no guarantee of future results.

Investment in Private Equity involves risks of liquidity and capital loss. Past performance is no guarantee of future results.

Performance

TRI or IRR

IRR is the Internal Rate of Return.

The net IRR is the IRR realized by a subscriber on his investment in a fund.

It considers:

The net IRR is the IRR realized by a subscriber on his investment in a fund.

It considers:

all (negative) flows relating to each successive capital call

all (positive) flows linked to (i) distributions and(ii) the estimated residual value of units held in the fund on the calculation date (known as the net asset value of units).

Unlike the multiple, it therefore incorporates the time effect.

Insofar as flows are full and net for the investor, this rate is net of management fees and carried interest.

The net asset value of a PE portfolio (otherwise known as Net Asset Value) is calculated as follows:

Insofar as flows are full and net for the investor, this rate is net of management fees and carried interest.

The net asset value of a PE portfolio (otherwise known as Net Asset Value) is calculated as follows:

by adding together the fair values of each of the companies held in the portfolio (as determined by the fund management company),

and deducting the value of portfolio liabilities and the theoretical carried interest due to the fund management team.

Unlike stock markets, the fair values of companies held by funds do not fluctuate daily. The two most commonly used methods for determining fair value are multiples and DCF (Discounted Cash-Flow).

Private Equity investments entail risks of liquidity and capital loss. Past performance is no guarantee of future results.

Private Equity investments entail risks of liquidity and capital loss. Past performance is no guarantee of future results.

Calculation method

Calculating Private Equity performance

The Altaroc offer

Discover our Private Equity ranges

Private Equity

Discovery

Institutional-quality Private Equity now available in French life insurance and PER - Assurance.

Minimum commitment

Amount defined by the insurer

Format

FCPR (venture capital fund) regulated by the AMF

Subscribers

Individuals

Private Equity

Odyssey

Every year, we build a highly diversified, high-performance, turnkey global Private Equity portfolio.

MINIMUM COMMITMENT

From €100,000

Format

Subscribers

Sophisticated retail or institutional investors

Private Equity

Infinity

Invest in private equity like the biggest institutional investors

A multi-million-dollar global private equity offering is in the pipeline.

Available soon

minimum commitment

undefined

Format

undefined

Subscribers

undefined

Private Equity news

FAQ

How do you explain the performance of Private Equity?

What are the risks of investing in Private Equity?