.webp)

Deciphering trends

Club Patrimoine - Retrocessions: A Turning Point for Market Practices?

To analyze the implications of this decision, assess its impact on the profession, and present Altaroc proposals, Club Patrimoine brought together Frédéric Stolar, CEO and co-founderAltaroc; David Charlet, President of ANACOFI; and Guillaume Goffin, Partner at Gide Loyrette Nouel.

Article

|

16

No items found.

No items found.

No items found.

Follow portfolio news

CookUnity surpasses $750 million in annual recurring revenue

Founded 10 years ago, CookUnity delivers meals prepared by renowned chefs directly to the homes of millions of customers. Featured in the Vintage FPCI Altaroc Odyssey , the New York-based company surpassed $750 million in annual recurring revenue in 2025.

Article

|

16

A must

North America

Consumption

No items found.

Odyssey 2021

CookUnity

CookUnity

Follow portfolio news

Easyfairs acquires two major trade shows in Paris

As a leading European trade show organizer, Easyfairs brings together more than 24,000 exhibitors and 1 million visitors each year across 110 diverse events. Featured in the Vintage FPCI Altaroc Odyssey , the Belgian organizer has just acquired two major Parisian events dedicated to innovation in the hospitality and retail sectors.

Article

|

16

Strong growth

Europe

Services

No items found.

Odyssey 2023

EasyFairs

EasyFairs

Follow portfolio news

HealthMark Group acquires a medical imaging specialist

With 20 million transfers processed, HealthMark Group is a leader in the digital distribution of medical images and records. As part of the Vintage FPCI Altaroc Odyssey portfolio, the U.S.-based company has just announced the acquisition of Purview, a cloud-based medical imaging company based in Annapolis, Maryland.

Article

|

16

Innovative

North America

Healthcare

No items found.

Odyssey 2023

HealthMark Group

HealthMark Group

Follow portfolio news

PEI Group acquires SIPA, a provider of data on private markets

Based in the United Kingdom, PEI Group provides a platform for storing and analyzing financial market data, used by more than 30,000 institutional investors. A portfolio company in the Vintage FPCI Altaroc Odyssey fund, the firm has just acquired Scientific Infra & Private Assets (SIPA), the world’s leading provider of indices, benchmarks, and ratings for the private infrastructure and private equity markets.

Article

|

16

Strong growth

North America

Technology / Software

No items found.

Odyssey 2022

PEI Group

PEI Group

Follow portfolio news

Vinted surpasses the €1 billion mark in revenue

Founded in 2008 in Lithuania, Vinted has established itself as Europe’s leading secondhand fashion platform. Featured in the Vintage FPCI Altaroc Odyssey , the unicorn with 80 million users has expanded into several European markets and generated over €1.1 billion in revenue in 2025.

Article

|

16

Unicorn

Europe

Consumption

No items found.

Odyssey 2021

Vinted

Vinted

Follow portfolio news

Athletic Brewing supports nature conservation

As the largest American brewer of non-alcoholic beer, Athletic Brewing distributes its products to 75,000 retail locations across the United States. Featured in the Vintage FPCI Altaroc Odyssey , the company is celebrating Earth Month with “Our Brews Give Back,” a campaign designed to donate the proceeds from its sales to projects dedicated to preserving nature.

Article

|

10

Strong growth

North America

Consumption

No items found.

Odyssey 2021

Athletic Brewing

Athletic Brewing

Follow portfolio news

Sun King is investing heavily to make solar energy more accessible in Ethiopia

With a presence in 46 countries across Africa, Asia, and South America, Sun King offers a wide range of solar panels and unique solar-powered products. As part of the Vintage FPCI Altaroc Odyssey fund, the American giant has just committed, alongside the Ethiopian Investment Commission, to investing $150 million to expand access to energy in Ethiopia through solar power.

Article

|

10

Positive impact

Rest of the world

Services

No items found.

Odyssey 2021

Sun King

Sun King

Follow portfolio news

Palex joins the United Nations Global Compact

With 80 years of experience, Palex distributes a wide range of medical equipment and technologies to hospitals in 12 European countries. Featured in the Vintage FPCI Altaroc Odyssey , the Spanish company has just reached a major milestone in its commitment to sustainability by joining the United Nations Global Compact.

Article

|

10

Innovative

Europe

Healthcare

No items found.

Odyssey 2022

Palex

Palex

Follow portfolio news

NationsBenefits adds 164 stores to its prepaid health card

With 150 million transactions per year, NationBenefits is a leader in payment services for healthcare and health products in the United States. The Florida-based company, which is part of the Vintage FPCI Altaroc Odyssey portfolio, has just announced a partnership with Food City, which operates 164 stores—including 120 pharmacies—across five U.S. states.

Article

|

10

Strong growth

North America

Healthcare

No items found.

Odyssey 2021

NationsBenefits

NationsBenefits

Follow portfolio news

80 Acres Farms Honored by Time and Forward Fooding

With its innovative vertical farms located across the United States, 80 Acres Farms is shaping the future of agriculture. Featured in the Vintage FPCI Altaroc Odyssey , the company—which sells its fruits and vegetables at Walmart, among other retailers—has just been recognized by the prestigious Time magazine and ranks second on the FoodTech 500 list.

Article

|

10

Positive impact

North America

Consumption

No items found.

Odyssey 2021

80 Acres Farms

80 Acres Farms

Follow portfolio news

One Inc: Modernizing Insurance Payments on a Large Scale

The insurance industry is built on a simple promise: to be able to provide prompt compensation in the event of a claim. Yet the payment infrastructure that underpins it often remains fragmented, under-digitized, and inefficient. This is precisely the problem that One Inc. is addressing.

Article

|

10

Innovative

Nordic Capital

No items found.

No items found.

No items found.

One Inc

One Inc

Follow portfolio news

IFS continues to make inroads into AI with the automation of transportation logistics

IFS, a global leader in operations management software for industrial companies such as TotalEnergies, is also a pioneer in AI-powered software. A portfolio company of the Vintage FPCI Altaroc Odyssey fund, the Swedish firm has just unveiled IFS.ai Logistics to automate transportation management for large enterprises.

Article

|

02

A must

Europe

Technology / Software

No items found.

Odyssey 2022

IFS

IFS

Follow portfolio news

Korean Air is modernizing its software infrastructure with IBS

More than 50 airlines already use IBS software to optimize cargo management, passenger services, crew management, and loyalty programs. Based in India and featured in the Vintage FPCI Altaroc Odyssey , the company was selected by Korean Air to modernize the management of its daily operations.

Article

|

02

Strong growth

Rest of the world

Technology / Software

No items found.

Odyssey 2022

IBS Software

IBS Software

Follow portfolio news

EcoVadis ranked among the world's most innovative companies

The French unicorn EcoVadis specializes in assessing the carbon footprint and social impact of major companies such as Amazon and LVMH. A portfolio company in the Vintage FPCI Altaroc Odyssey fund, the company was named one of the world’s most innovative companies by Fast Company, a leading U.S. media outlet covering innovation.

Article

|

02

Unicorn

Europe

Services

No items found.

Odyssey 2021

EcoVadis

EcoVadis

Follow portfolio news

DeepIntent speeds up the launch of healthcare marketing campaigns by 50%

Founded in 2016 in New York, DeepIntent enables healthcare companies and agencies to design and measure the performance of their digital ads. Featured in the Vintage FPCI Altaroc Odyssey portfolio, the U.S.-based company has just announced the launch of Helix, a tool that helps healthcare industry players better manage and measure their advertising campaigns.

Article

|

02

Innovative

North America

Technology / Software

No items found.

Odyssey 2024

DeepIntent

DeepIntent

Follow portfolio news

Cleerly enables the early detection of cardiovascular diseases using AI

Cardiovascular disease accounts for one in five deaths in the United States. To address this issue, Cleerly has developed an AI system trained on 10 million images, capable of assisting cardiologists and detecting early warning signs sooner. Featured in the Vintage FPCI Altaroc Odyssey , Cleerly assists Dr. Kevin Young, a leading advocate for cardiovascular disease awareness.

Article

|

02

Innovative

North America

Healthcare

No items found.

Odyssey 2025

Cleerly

Cleerly

Deciphering trends

Distributing Private Equity in Banking: The Key Challenge of Client Support

Private equity doesn't have a problem with appetite, but with execution. Private equity is going through a major evolutionary phase. Long reserved for institutional investors (pension funds, insurers, Family Office ), it is gradually opening up to a wider wealth management clientele, seeking diversification, performance uncorrelated with listed markets and long-term investment solutions.

Article

|

02

No items found.

No items found.

No items found.

Odyssey 2025

Follow portfolio news

VectorY Therapeutics has been approved by the U.S. Food and Drug Administration for its treatment of Charcot’s disease

Based in Amsterdam, VectorY Therapeutics develops innovative treatments for people with rare genetic diseases. The company, which is part of the Vintage FPCI Altaroc Odyssey portfolio, announced that the FDA, the U.S. health authority, had granted it a special designation to accelerate the development of its treatment for Charcot’s disease.

Article

|

20

Positive impact

Europe

Healthcare

No items found.

Odyssey 2021

VectorY Therapeutics

VectorY Therapeutics

Follow portfolio news

Coalfire streamlines compliance for tech companies

Based in Chicago, Coalfire supports more than 1,000 software companies with a comprehensive and robust cybersecurity framework. As part of theOdyssey FPCI Altaroc Odyssey Vintage portfolio, the company is partnering with Drata—which automates compliance for global leaders such as OpenAI and LinkedIn—to transform manual security audits into a continuous, AI-driven certification process.

Article

|

20

Strong growth

North America

Technology / Software

No items found.

Odyssey 2021

Coalfire

Coalfire

Follow portfolio news

Aeris is improving the management of 10,000 connected devices at Swiss International Airlines

Based in San Jose, California, Aeris helps companies connect and manage physical devices via the internet, anywhere in the world. Featured in the Vintage FPCI Altaroc Odyssey , the company has enabled Swiss International Airlines to significantly improve visibility and control over its 10,000 connected devices, while enhancing operational safety.

Article

|

20

Innovative

North America

Technology / Software

No items found.

Odyssey 2023

Aeris

Aeris

Follow portfolio news

BrowserStack Named Best Software Company in India

BrowserStack helps 50,000 companies test their web and mobile apps to identify bugs. A portfolio company in the Vintage FPCI Altaroc Odyssey fund, the Indian unicorn was named the Best Software Company in India by the prestigious G2 ranking.

Article

|

20

Unicorn

Rest of the world

Technology / Software

No items found.

Odyssey 2021

Browserstack

Browserstack

Follow portfolio news

Hawkeye 360 Selected for a Major European Technology Program

Hawkeye 360’s 36 satellites in orbit analyze radio frequency signals around the world, primarily for defense and intelligence purposes. Based in Virginia and featured in the Vintage FPCI Altaroc Odyssey , the company has just announced that it has been selected by a European defense ministry as part of a major technology development program.

Article

|

20

Strong growth

North America

Europe

Technology / Software

No items found.

Odyssey 2021

HawkEye 360

HawkEye 360

.webp)

Follow portfolio news

Ideagen Named Best Software Solution for the Third Consecutive Year

More than 18,500 companies operating in regulated sectors such as aerospace and food processing have entrusted Ideagen with the management and security of their processes and products. Featured in the Vintage FPCI Altaroc Odyssey portfolio, the Nottingham-based company has been named among the top 50 software companies in the UK for the third consecutive year.

Article

|

19

Innovative

Europe

Technology / Software

No items found.

Odyssey 2022

Ideagen

Ideagen

Follow portfolio news

Fresha resolves 80% of customer support tickets automatically

With over a billion appointments booked across 120 countries, Fresha is the world’s leading booking platform for beauty and wellness services. The London-based company, which is part of the Vintage FPCI Altaroc Odyssey portfolio, has just announced that 80% of customer support tickets are now resolved automatically by its AI, Nova.

Article

|

19

Innovative

Europe

Services

No items found.

Odyssey 2021

Fresha

Fresha

Follow portfolio news

Datassential is enhancing its technology for the restaurant industry

Founded in 2001 in Chicago, Datassential is a leader in data analytics for the food and beverage industry. Featured in the Vintage FPCI Altaroc Odyssey , the company has just announced the release of new capabilities integrated into Datassential One, its AI tool designed to simplify data in an increasingly complex industry.

Article

|

19

A must

North America

Technology / Software

No items found.

Odyssey 2023

Datassential

Datassential

Follow portfolio news

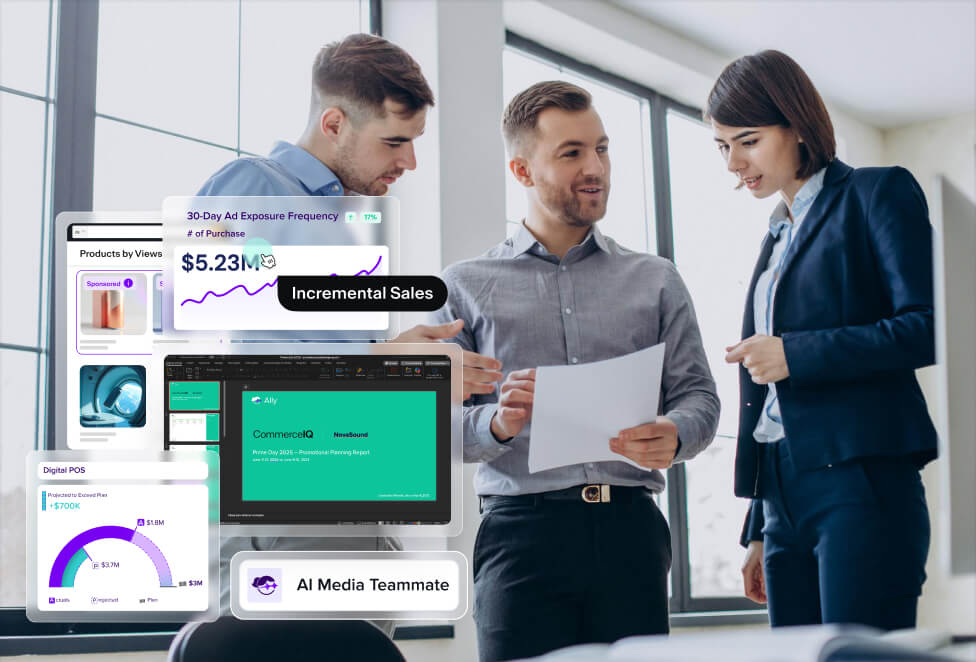

Online Sales: CommerceIQ Unveils 4 New AI Agents

CommerceIQ helps more than 2,200 brands, including Nestlé and Colgate, optimize their online sales through real-time data analytics. A portfolio company in the Vintage FPCI Altaroc Odyssey fund, the California-based company has just announced the launch of the e-commerce sector’s first suite of AI agents, which already deliver performance 10 to 100 times better than human analysis alone.

Article

|

19

Unicorn

North America

Technology / Software

No items found.

Odyssey 2021

CommerceIQ

CommerceIQ

Follow portfolio news

Canary Technologies partners with the luxury group Beaumier Hotels to enhance the guest experience

Canary Technologies, a digital platform designed for hotels worldwide, supports more than 20,000 properties in 100 countries. As part of the Vintage FPCI Altaroc Odyssey portfolio, the California-based company has added Beaumier Hotels—a chain of 10 luxurious and unique hotels located across Europe—to its client roster.

Article

|

19

Innovative

North America

Technology / Software

No items found.

Odyssey 2021

Canary Technologies

Canary Technologies

Follow portfolio news

Chess.com now has 250 million users

Just under a year ago, in May 2025, Chess.com surpassed the 200-million-user mark. Ten months later, the company—which is part of the Vintage FPCI Altaroc Odyssey —has attracted another 50 million users, signaling a new wave of chess enthusiasts.

Article

|

13

A must

North America

Technology / Software

No items found.

Odyssey 2021

Chess.com

Chess.com

Follow portfolio news

Coupa has delivered over $300 billion in savings for its customers

For the past 20 years, Coupa has been helping companies like Mastercard, Uber, and Nike reduce their expenses by optimizing their procurement and invoicing processes. Part of the Vintage FPCI Altaroc Odyssey portfolio, the American unicorn has just released its Q4 2025 results and has surpassed the symbolic milestone of $300 billion in savings for its clients.

Article

|

13

Unicorn

North America

Technology / Software

No items found.

Odyssey 2021

Coupa

Coupa

Follow portfolio news

Plusgrade partners with China Airlines

Based in Canada, Plusgrade is a leader in the travel industry, helping hotels, restaurants, and transportation companies generate additional revenue. Featured in the Vintage FPCI Altaroc Odyssey , Plusgrade is partnering with China Airlines to launch new products for the airline’s frequent flyers.

Article

|

13

A must

North America

Services

No items found.

Odyssey 2021

PlusGrade

PlusGrade

Follow portfolio news

Visma generated €2.8 billion in revenue in 2025.

With nearly 30 acquisitions in 2025, Visma continues to grow. The Norwegian company, which is a co-investment in the Vintage FPCI Altaroc Odyssey fund, reported revenue of €2.8 billion, up 17%. Alongside the release of its 2025 results, the Norwegian company has just announced the acquisition of Brazil’s largest platform for micro-entrepreneurs.

Article

|

13

A must

Europe

Services

No items found.

Odyssey 2023

Visma

Visma

Understanding Private Equity

Evergreen and secondary market: towards a structural evolution of private equity

Evergreen funds now represent nearly $400 billion in assets under management* worldwide. Initially considered complementary to traditional closed-end funds, they are gradually becoming established in strategic allocations, including institutional ones.

Article

|

16

No items found.

No items found.

No items found.

Discover Altaroc

Introducing the 6th Vintage the Odyssey line

Watch the recording of our webinar introducing the upcoming Vintage edition Vintage the Odyssey line

Article

|

24

No items found.

No items found.

No items found.

Odyssey 2026

Follow portfolio news

80 Acres Farms raises awareness about vertical farms at the UN

Based in Ohio, 80 Acres Farms is a pioneer in Agriculture 2.0—a technology-driven and environmentally friendly approach to farming. Featured in theOdyssey FPCI Altaroc Odyssey Vintage , the American company had the opportunity to promote vertical farming as an alternative to traditional agriculture at the United Nations.

Article

|

05

Positive impact

North America

Consumption

No items found.

Odyssey 2021

80 Acres Farms

80 Acres Farms

Follow portfolio news

Flo Health can detect endometriosis 50% faster

Flo Health, the world’s most downloaded period tracking app, has been improving women’s health for 10 years. The London-based unicorn, which is part of the Vintage FPCI Altaroc Odyssey portfolio, has just released the results of a study suggesting that, with proper tracking on the app, endometriosis could be detected four years earlier.

Article

|

05

Positive impact

Europe

Healthcare

No items found.

Odyssey 2021

Flo Health

Flo Health

Follow portfolio news

Employee benefits: NationsBenefits partners with 97 Kinney Drugs pharmacies

With 150 million transactions per year, NationBenefits is a leader in health benefits management for Americans. A portfolio company of the Vintage FPCI Altaroc Odyssey fund, the company is partnering with Kinney Drugs, which operates more than 100 pharmacies in New York State and Vermont.

Article

|

05

Strong growth

North America

Healthcare

No items found.

Odyssey 2021

NationsBenefits

NationsBenefits

Follow portfolio news

Care for the elderly: Innovage met with Colorado State legislators

Based in Denver, Colorado, Innovage is a leading provider of senior care, enabling older adults to receive care in their own homes. The company, which is part of the Vintage FPCI Altaroc Odyssey portfolio, met with several lawmakers at the Colorado State Capitol to highlight the importance of strengthening care for the state’s aging population, which numbers no fewer than 6 million residents, 15% of whom are seniors.

Article

|

05

Innovative

North America

Healthcare

No items found.

Odyssey 2021

InnovAge

InnovAge

Follow portfolio news

Sun King unveils three new products designed to improve the daily lives of millions of Africans

More than 25 million households in Africa and Southeast Asia already have access to solar energy thanks to Sun King. The company, which is part of the Vintage FPCI Altaroc Odyssey fund, has just unveiled a new line of products designed to improve the daily lives of millions of people, while continuing to create jobs across the African continent.

Article

|

05

Positive impact

Rest of the world

Consumption

No items found.

Odyssey 2021

Sun King

Sun King

Follow portfolio news

Vector Solutions is committed to training volunteer firefighters

For more than 25 years, Vector Solutions has been protecting millions of employees in critical industries through its SaaS-based training and decision-support software. A portfolio company of the Vintage FPCI Altaroc Odyssey fund and based in Florida, the company has just unveiled a training platform for volunteer firefighters.

Article

|

20

Innovative

North America

Technology / Software

No items found.

Odyssey 2021

Vector Solutions

Vector Solutions

Follow portfolio news

Breast cancer detection: study confirms reliability of Screenpoint Medical's AI

Based in the Netherlands, ScreenPoint Medical has developed Transpara Breast, an AI system capable of improving the early detection of breast cancer and thereby saving many lives. The company, which is part of the Vintage FPCI Altaroc Odyssey portfolio, has just published the results of its latest study, which confirms the reliability of its technology by detecting 29% more cancers.

Article

|

20

Positive impact

Europe

Healthcare

No items found.

Odyssey 2021

ScreenPoint

ScreenPoint

.webp)

Follow portfolio news

MiQ transforms digital advertising with Sigma

As a global leader in advertising campaign optimization, MiQ works with some of the world’s top marketing specialists (Vizio, Google). Featured in the Vintage FPCI Altaroc Odyssey , the British leader has just launched Sigma, a new AI-powered digital advertising solution.

Article

|

20

Innovative

Europe

Technology / Software

No items found.

Odyssey 2022

MiQ

MiQ

Follow portfolio news

Marlink to equip France's leading shipping company

Based in Paris, Marlink is the world’s leading satellite communications provider for the merchant marine and cruise industry. A portfolio company of the Vintage FPCI Altaroc Odyssey fund, the company—with 75 years of experience—has been selected by CMA CGM to install a new communications system on 350 of its vessels.

Article

|

20

A must

Europe

Technology / Software

No items found.

Odyssey 2021

Marlink

Marlink

Follow portfolio news

Empyrean rolls out behavioral analytics tool for banks

For the past 18 years, Empyrean has been supporting finance departments and banks by making financial data easier to interpret and interest rates easier to understand. The U.S.-based company, which is part of the Vintage FPCI Altaroc Odyssey portfolio, has just launched Model IQ, a behavioral modeling platform designed to help banks better anticipate how their customers will react to economic fluctuations.

Article

|

20

Innovative

North America

Technology / Software

No items found.

Odyssey 2022

Empyrean Solutions

Empyrean Solutions

Follow portfolio news

Staffbase strengthens its presence in Central America

Based in Germany, Staffbase has developed a unique platform to boost employee engagement at its clients, including Adidas, Toyota, and Mercedes-Benz. Given the growing demand for its solutions, Staffbase—a portfolio company of the Vintage FPCI Altaroc Odyssey fund—has announced the opening of an office in Mexico City.

Article

|

19

Unicorn

Europe

Technology / Software

No items found.

Odyssey 2021

Staffbase

Staffbase

Follow portfolio news

Septeo acquires its German counterpart

As the French leader in software for the legal, real estate, and IT sectors, Septeo now serves more than 200,000 users across Europe. Headquartered in Occitanie and backed by the Vintage FPCI Altaroc Odyssey fund, the French unicorn has just acquired stp.one, its German counterpart.

Article

|

19

Positive impact

Europe

Technology / Software

No items found.

Odyssey 2022

Septeo

Septeo

Follow portfolio news

Ivalua ended 2025 with solid performance

Founded 25 years ago in France, Ivalua has developed a unique cloud-based expense management platform, now used by Volkswagen, Booking.com, and Crédit Agricole. As part of the Vintage FPCI Altaroc Odyssey portfolio, the company continued to grow in 2025, with a 24% increase in subscription revenue.

Article

|

19

Innovative

Europe

Technology / Software

No items found.

Odyssey 2022

Ivalua

Ivalua

Follow portfolio news

IFS reports strong growth in 2025

Air France-KLM, TotalEnergies, and Rolls-Royce use IFS for its unique cloud platform, designed to streamline and manage all day-to-day operations in these heavily regulated industries. Co-invested in the Vintage FPCI Altaroc Odyssey fund, the Swedish company reported a 23% increase in its annual recurring revenue in 2025 and a 30% increase in its cloud revenue.

Article

|

19

A must

Europe

Technology / Software

No items found.

Odyssey 2022

IFS

IFS

Follow portfolio news

Cary Group recorded a 31% increase in revenue in 2025.

As the European leader in automotive glass replacement, Cary Group operates in 13 countries thanks to a highly active expansion and acquisition strategy. Featured in the Vintage FPCI Altaroc Odyssey , the Swedish company, with 70 years of experience, has just reported strong financial growth for 2025.

Article

|

19

A must

Europe

Services

No items found.

Odyssey 2021

Cary Group

Cary Group

Follow portfolio news

FloQast exceeds $200 million in annual recurring revenue

Used by Zoom, SumUp, and Shopify, FloQast automates and simplifies accounting workflow management. Based in Los Angeles and part of the Vintage FPCI Altaroc Odyssey portfolio, the company has just surpassed the symbolic milestone of $200 million in annual recurring revenue (ARR), a sign of the growing and sustained adoption of its solutions.

Article

|

12

Strong growth

North America

Technology / Software

No items found.

Odyssey 2021

Floqast

Floqast

Follow portfolio news

Foxway expands into Eastern Europe to refurbish even more devices

Based in Sweden, Foxway helped prevent the emission of nearly 10 tons of CO₂ in 2025 by repairing and refurbishing electronic devices for businesses. The company, which is part of the Vintage FPCI Altaroc Odyssey portfolio, has just acquired ABD, a Romanian firm specializing in the restoration of complex electronic devices.

Article

|

12

Positive impact

Europe

Technology / Software

No items found.

Odyssey 2021

Foxway

Foxway

Follow portfolio news

DriveWealth recorded 8.56 million trades in one day.

Founded in 2012 in New Jersey, DriveWealth simplifies access to financial markets for individual investors through interfaces that allow apps to directly integrate investment services. A portfolio company in the Vintage FPCI Altaroc Odyssey fund, DriveWealth has just reached a major milestone: its platform processed 8.56 million transactions in a single day.

Article

|

12

Unicorn

North America

Services

No items found.

Odyssey 2021

DriveWealth

DriveWealth

Follow portfolio news

CommerceIQ partners with Acosta Group to optimize sales for thousands of businesses

Based in California and valued at over $1 billion, CommerceIQ helps companies such as Nestlé, Colgate, and Whirlpool optimize their online sales. A portfolio company of the Vintage FPCI Altaroc Odyssey fund, the company has just entered into a partnership with Acosta Group, a U.S. specialist in retail sales and product promotion with nearly a century of experience.

Article

|

12

Unicorn

North America

Services

No items found.

Odyssey 2021

CommerceIQ

CommerceIQ

Follow portfolio news

Access Group expands its offering with the acquisition of MaxOptra

With more than 160,000 corporate clients worldwide, Access Group is a UK leader in business software for mid-market companies, serving customers from the UK to North America and the Asia-Pacific region. Co-invested in the Vintage FPCI Altaroc Odyssey fund, Access Group has just acquired MaxOptra, a British platform for delivery and fleet management.

Article

|

12

Unicorn

Europe

Technology / Software

No items found.

Odyssey 2022

The Access Group

The Access Group

Follow portfolio news

Vinted launches in the United States

Founded in 2008, the Lithuanian unicorn quickly conquered the European secondhand market, starting with clothing and now expanding into books and electronics. Featured in the Vintage FPCI Altaroc Odyssey , Vinted is now expanding into the United States and setting up shop in New York.

Article

|

09

Unicorn

Europe

Consumption

No items found.

Odyssey 2021

Vinted

Vinted

Follow portfolio news

Vector Solutions launches sixth annual Firefighter Cancer Awareness Month

For 25 years, Vector Solutions has been supporting public and industrial sectors with its training, workforce management, and operational readiness solutions. The Florida-based company, which is part of the Vintage FPCI Altaroc Odyssey portfolio, has launched the 6th edition of Firefighter Cancer Awareness Month, offering free webinars, training, and resources designed to reduce the risk of cancer among firefighters.

Article

|

09

Innovative

North America

Technology / Software

No items found.

Odyssey 2021

Vector Solutions

Vector Solutions

Follow portfolio news

FloQast named one of the Best Places to Work for the eighth consecutive year

Revolut, SoundCloud, Emma, and Get Your Guide are just a few of the companies using FloQast to automate their accounting processes. Based in Los Angeles and part of the Vintage FPCI Altaroc Odyssey portfolio, FloQast has been named one of the “Best Places to Work” among mid-sized companies in Chicago and Los Angeles for the eighth consecutive year.

Article

|

09

Strong growth

North America

Technology / Software

No items found.

Odyssey 2021

Floqast

Floqast

Follow portfolio news

EcoVadis becomes a search criterion on Amazon Business

Founded in 2007 in Paris, EcoVadis has established itself as the leader in assessing the CSR performance of companies worldwide, with clients such as Lenovo, Longchamp, and HSBC. The French unicorn, which is part of the Vintage FPCI Altaroc Odyssey fund, has just become a key search criterion on Amazon Business, the American giant’s corporate procurement solution.

Article

|

09

Unicorn

Europe

Services

No items found.

Odyssey 2021

EcoVadis

EcoVadis

Follow portfolio news

80 Acres Farms products now available nationwide

Based in Ohio, 80 Acres Farms is reinventing agriculture through connected indoor vertical farms. The American company, which is part of the Vintage FPCI Altaroc Odyssey portfolio, has just reached a major milestone in its development. Its fresh, healthy, and sustainable products are now available in all 50 states.

Article

|

29

Positive impact

North America

Consumption

No items found.

Odyssey 2021

80 Acres Farms

80 Acres Farms

Follow portfolio news

Sedna and StormGeo join forces to simplify maritime operations

Sedna offers maritime transport and logistics companies a centralized communication platform that consolidates and organizes all operational communications. The London-based company, which is part of the Vintage FPCI Altaroc Odyssey portfolio, has partnered with StormGeo, a provider of weather-based transportation solutions.

Article

|

29

Innovative

Europe

Technology / Software

No items found.

Odyssey 2021

Sedna

Sedna

Follow portfolio news

Dental care 2.0: Overjet partners with Medit

Founded in Harvard’s innovation labs in 2018, Overjet is the leader in AI-powered dental analysis. A portfolio company of the Vintage FPCI Altaroc Odyssey fund, Overjet is partnering with Medit, a South Korean provider of 3D oral scanners operating in over 100 countries.

Article

|

29

Strong growth

North America

Healthcare

No items found.

Odyssey 2021

Overjet

Overjet

Follow portfolio news

Flo Health wins award at Google Play Awards in Southeast Asia

With over 43 million active users, Flo Health is the world’s most downloaded app for women’s health and menstrual cycle tracking. Based in London and part of the Vintage FPCI Altaroc Odyssey portfolio, the company has just won the Google Play “Best of 2025” award in the “Best Smartwatch App” category in Hong Kong, Taiwan, and Macau.

Article

|

29

Positive impact

Europe

Consumption

No items found.

Odyssey 2021

Flo Health

Flo Health

Follow portfolio news

DataSnipper generated $1.4 billion in productivity gains for its customers in 2025.

Based in Amsterdam, DataSnipper has developed a platform that automates audit procedures, eliminates 90% of manual tasks, and reduces operating costs by 50%. The Dutch company, which is part of the Vintage FPCI Altaroc Odyssey portfolio, ended 2025 having generated more than $1.4 billion in productivity gains for its clients worldwide.

Article

|

29

Innovative

Europe

Technology / Software

No items found.

Odyssey 2021

DataSnipper

DataSnipper

%2520Canary.jpeg)

Follow portfolio news

Canary Technologies wins in 10 categories as best hotel technology platform

San Francisco-based Canary Technologies was recognized in 10 categories as the best hotel technology by more than 25,000 industry professionals worldwide. Featured in the Vintage FPCI Altaroc Odyssey , the company was honored at the HotelTechAwards, which annually recognize the best technology solutions used by hotels, with winners selected based on verified reviews from hoteliers.

Article

|

29

Innovative

North America

Services

No items found.

Odyssey 2021

Canary Technologies

Canary Technologies

Follow portfolio news

Two new acquisitions for Cary Group

With over 70 years of experience, Cary Group is a leading provider of automotive glass repair and replacement services in 12 European countries. As part of its efforts to expand its service offerings and geographic reach, the Swedish company, which is participating in the Vintage FPCI Altaroc Odyssey , is pursuing an active growth strategy, already marked by some thirty acquisitions in Europe, with the recent purchase of two new companies.

Article

|

22

A must

Europe

Services

No items found.

Odyssey 2021

Cary Group

Cary Group

Follow portfolio news

team.blue acquires Swiss platform specializing in data integration

With a presence in 22 countries, team.blue is one of Europe’s leading providers of online hosting services for small and medium-sized businesses. Based in Belgium and backed by the Vintage FPCI Altaroc Odyssey fund, team.blue has just acquired Windsor.ai, a Swiss company that helps its clients make smarter marketing decisions by analyzing all their data.

Article

|

22

Unicorn

Europe

Technology / Software

No items found.

Odyssey 2022

Team.blue

Team.blue

Follow portfolio news

Nulo rolls out its premium pet food in the United Kingdom

With dog and cat food rich in animal protein and low in carbohydrates, Nulo helps reduce the risk of diabetes in our four-legged friends while improving their health with a variety of probiotics. Based in Austin, Texas, and featured in theOdyssey FPCI Altaroc Odyssey Vintage , the company is making its debut in Europe with a launch in the United Kingdom.

Article

|

22

A must

North America

Consumption

No items found.

Odyssey 2021

Nulo

Nulo

Follow portfolio news

Fireblocks acquires TRES Finance and structures crypto accounting

Based in New York, Fireblocks offers cutting-edge expertise and an innovative approach to help the 2,400 companies that use its services—including Revolut, Visa, and BNP Paribas—manage the day-to-day operations of their digital assets (storage, transfers, and issuance). A portfolio company in the Vintage FPCI Altaroc Odyssey fund, the company has just acquired TRES Finance, a platform that automates reconciliation, reporting, and accounting across more than 280 blockchains, exchanges, banks, and custodians.

Article

|

22

Unicorn

North America

Services

No items found.

Odyssey 2021

Fireblocks

Fireblocks

Follow portfolio news

Kevin Hart teams up with Authentic Brands Group to develop his brand

Kevin Hart, a renowned American actor best known for his roles in *The Upside* and the *Jumanji* franchise, has just entered into a partnership with Authentic Brands Group. The American company, which is part of the Vintage FPCI Altaroc Odyssey portfolio, owns more than 50 fashion and entertainment brands, including Champion, Dockers, and Reebok.

Article

|

22

Strong growth

North America

Consumption

No items found.

Odyssey 2021

Authentic Brands Group

Authentic Brands Group

Follow portfolio news

Opteven expands into Portugal

Based in Lyon, Opteven is one of Europe’s leading providers of mechanical breakdown coverage. As a portfolio company of the Vintage FPCI Altaroc Odyssey fund, Opteven now operates in 13 European countries following its acquisition of Conexão Garantias in Portugal.

Article

|

08

Strong growth

Europe

Services

No items found.

Odyssey 2021

Opteven

Opteven

Follow portfolio news

Clinical trials: ObjectiveHealth acquires Piedmont Research Partners

ObjectiveHealth, which operates in 16 U.S. states, has developed software solutions designed to speed up the identification and recruitment of patients for clinical trials. A portfolio company in the Vintage FPCI Altaroc Odyssey fund, ObjectiveHealth has just acquired Piedmont Research Partners, a well-established center based in Indian Land, South Carolina, to accelerate clinical trials and improve patient access to medical research.

Article

|

08

Positive impact

North America

Healthcare

No items found.

Odyssey 2024

ObjectiveHealth

ObjectiveHealth

Follow portfolio news

team.blue acquires Macaly to facilitate the creation of web applications

team.blue, based in Ghent, Belgium, helps European SMEs create, host, and operate their websites and web applications. A portfolio company of Vintage FPCI Altaroc Odyssey , the company has just acquired Macaly, a Czech developer of AI-powered web applications.

Article

|

08

Unicorn

Europe

Technology / Software

No items found.

Odyssey 2022

Team.blue

Team.blue

Follow portfolio news

Databricks surpasses $134 billion valuation

Based in San Francisco, Databricks helps more than 60% of Fortune 500 companies analyze their data. A portfolio company in the Vintage FPCI Altaroc Odyssey fund, the American unicorn has just raised $4 billion from several investors, including Insight Partners, bringing its valuation to $134 billion.

Article

|

08

Unicorn

North America

Technology / Software

No items found.

Odyssey 2021

Databricks

Databricks

Follow portfolio news

ASG Eye Hospitals plans to open 500 additional centers by 2030

With more than 175 specialized hospitals in 95 cities, ASG Eye Hospitals is one of India’s largest networks of state-of-the-art eye care facilities. Part of the Vintage FPCI Altaroc Odyssey portfolio, ASG Eye Hospitals has just unveiled a $240 million expansion plan and aims to have 700 specialized centers in India by 2030.

Article

|

08

Innovative

Rest of the world

Healthcare

No items found.

Odyssey 2021

ASG Eye Hospitals

ASG Eye Hospitals

Follow portfolio news

VAST Data and Nvidia collaborate to remove bottlenecks associated with managing massive amounts of data

VAST Data, which already partners with Microsoft, Meta, and OpenAI, is now teaming up with Nvidia, the first company to surpass a $5 trillion market valuation. As part of the Vintage FPCI Altaroc Odyssey portfolio, VAST Data aims to eliminate barriers to data access and management.

Article

|

08

Unicorn

North America

Technology / Software

No items found.

Odyssey 2021

Vast Data

Vast Data

Follow portfolio news

Road transport: Motive's AI is now saving lives in Canada and Mexico

Motive is launching its AI solution in Canada and Mexico, which has the potential to save the lives of many drivers. Based in San Francisco and part of the Vintage FPCI Altaroc Odyssey portfolio, Motive enhances the reliability of corporate fleets through the use of smart onboard cameras and optimized route planning. The California-based company is expanding its partnership with RapidSOS, which works with thousands of emergency centers across North America.

Article

|

08

Unicorn

North America

Technology / Software

No items found.

Odyssey 2021

Motive

Motive

Follow portfolio news

Cirque du Soleil dazzles Hawaii with ‘Auna

It is on the island of Oahu, in Honolulu, that Cirque du Soleil—featured in the Vintage FPCI Altaroc Odyssey —is currently performing “Auana,” a permanent show designed to celebrate Hawaiian culture and history through an immersive visual and artistic experience.

Article

|

08

A must

North America

Consumption

No items found.

Odyssey 2021

Cirque du Soleil

Cirque du Soleil

Follow portfolio news

BrowserStack launches AI to analyze app test failures on mobile devices

BrowserStack, an Indian unicorn and global leader in mobile and web application testing, has just launched a new AI-powered test failure analysis agent. As part of the Vintage FPCI Altaroc Odyssey portfolio, BrowserStack aims to speed up and improve the reliability of the 3 million application tests it performs every day for clients such as Google, Microsoft, and Nvidia.

Article

|

08

Unicorn

Rest of the world

Technology / Software

No items found.

Odyssey 2021

Browserstack

Browserstack

Follow portfolio news

Astronomer makes Pittsburgh city data accessible to its 300,000 residents

Based in Cincinnati and used by Walmart and Société Générale, Astronomer has developed a platform that automates the collection, processing, and distribution of data in real time. As part of the Vintage FPCI Altaroc Odyssey portfolio, the company has put its technology to work for the 300,000 residents of Pittsburgh, Pennsylvania, enabling them to view construction projects, building permits, inspections, and reported issues in their city instantly online.

Article

|

08

Innovative

North America

Technology / Software

No items found.

Odyssey 2021

Astronomer

Astronomer

Deciphering trends

Cressey & Company a long-term sector-based approach to transforming the healthcare industry

In an interview conducted at the offices of Cressey & Company Chicago, David Rogero, Managing Partner, discusses the firm's DNA, its investment strategy, and its vision for the evolution of the healthcare sector in North America.

Article

|

08

Cressey & Company

No items found.

Healthcare

No items found.

Follow portfolio news

Shift5 chosen by the US Army to modernize the F-16 data processing system

Shift5’s mission is to protect transportation infrastructure and armed forces around the world. Featured in the Vintage FPCI Altaroc Odyssey , the American company has just secured a strategic contract with the U.S. Air Force to modernize the F-16 Fighting Falcon, the world’s most widely used fighter jet.

Article

|

23

Innovative

North America

Technology / Software

No items found.

Odyssey 2021

Shift5

Shift5

Follow portfolio news

Visma strengthens its growth with the acquisition of Alavie and increased quarterly results

Visma, Europe’s leading provider of cloud-based business software, has just acquired Alavie, an Italian company specializing in regulatory compliance. At the same time, the Norwegian giant, a co-investor in the Vintage FPCI Altaroc Odyssey fund, reported strong results for the third quarter of 2025, with revenue of €2.33 billion (+13%).

Article

|

23

A must

Europe

Services

No items found.

Odyssey 2023

Visma

Visma

Follow portfolio news

Roller raises $50 million

Roller is taking another step forward in its growth with a $50 million funding round aimed at accelerating the development of its solutions for amusement parks and players in the tourism industry. A portfolio company of the Vintage FPCI Altaroc Odyssey fund, the U.S.-based company processes $4 billion in transactions on its platform each year and generates 5 million bookings per month.

Article

|

23

A must

North America

Technology / Software

No items found.

Odyssey 2021

Roller

Roller

Follow portfolio news

Easyfairs makes its first acquisition in North America with EPC

Easyfairs ranks among the top 10 trade show organizers worldwide. Headquartered in Belgium and participating in the Vintage FPCI Altaroc Odyssey , the company has just made its first acquisition in North America by purchasing EPC, a trade show dedicated to major energy projects that brings together industry giants such as Amazon and NVIDIA.

Article

|

23

Strong growth

Europe

Services

No items found.

Odyssey 2023

EasyFairs

EasyFairs

Follow portfolio news

IFS signs agreement to acquire U.S. counterpart Softeon

IFS, a global leader in management software for industrial companies, has just signed an agreement to acquire Softeon, its U.S. counterpart. As a co-investor in the Vintage FPCI Altaroc Odyssey fund and headquartered in Sweden, IFS aims to expand its product portfolio with a focus on supply chains.

Article

|

23

A must

Europe

Technology / Software

No items found.

Odyssey 2022

IFS

IFS

Follow portfolio news

Coupa partners with NGOs to automate their workflows and resources

Part of the Vintage FPCI Altaroc Odyssey portfolio, Coupa helps U.S. small and medium-sized businesses manage their payroll, human resources, and employee retirement benefits. The California-based company now works with NGOs such as Save the Children International to streamline their operations, reduce administrative costs, and devote more resources to their social mission.

Article

|

22

Unicorn

North America

Technology / Software

No items found.

Odyssey 2021

Coupa

Coupa

Follow portfolio news

IRIS Software certified as a Great Place to Work for the sixth consecutive year in the United Kingdom

IRIS Software has just been certified as a Great Place to Work for the sixth consecutive year in the United Kingdom, while also renewing its certifications in the United States, Canada, and Romania. The UK-based company, in which Vintage FPCI Altaroc Odyssey holds a stake, provides software solutions and services for finance, HR, and payroll teams in more than 130 countries.

Article

|

22

Strong growth

Europe

Technology / Software

No items found.

Odyssey 2023

Iris Software

Iris Software

Follow portfolio news

Cary Group aims for carbon neutrality by 2050

As a European leader specializing in sustainable solutions for vehicle glass repair and replacement, Cary Group is strengthening its climate ambition by officially committing to the SBTi Net-Zero Standard (defined by the IPCC). The goal of the Swedish company, which is part of the Vintage FPCI Altaroc Odyssey portfolio, is to achieve carbon neutrality across its entire value chain by 2050.

Article

|

22

A must

Europe

Services

No items found.

Odyssey 2021

Cary Group

Cary Group

Follow portfolio news

Beewise recognized among the 100 companies shaping a sustainable future

Based in California and featured in theOdyssey Vintage FPCI Altaroc Odyssey , Beewise was recognized in the World Future Awards’ Top 100 Next Generation Companies ranking. Compiled by an international organization, this ranking highlights the most innovative companies committed to building a better future.

Article

|

22

Positive impact

Rest of the world

Technology / Software

No items found.

Odyssey 2021

Beewise

Beewise

Follow portfolio news

Sun King raises $40 million to accelerate solar energy deployment in Africa

A recognized leader in solar power in Africa, Sun King has just raised $40 million from Lightrock (Fund manager private equityFund manager ) to accelerate the deployment of its off-grid solutions. This new round of funding is part of Sun King’s commitment—the company is part of the Vintage FPCI Altaroc Odyssey fund—to provide the entire African continent with affordable access to clean and reliable energy.

Article

|

22

Positive impact

Rest of the world

Consumption

No items found.

Odyssey 2021

Sun King

Sun King

Discover Altaroc

Altaroc Compliance team, a reliable and trustworthy partner

Since joining the company in 2024 as Director of Compliance, Internal Control, and Risk, Diana Valier has been working to structure and strengthenAltaroc culture of rigor.

Article

|

19

No items found.

No items found.

No items found.

Follow portfolio news

250,000 Californians gain access to therapeutic meals thanks to CookUnity

Nearly 250,000 residents of Sacramento are now eligible to receive fresh, chef-prepared meals delivered to their homes. CookUnity is partnering with Anthem Blue Cross, one of the leading health insurers in the United States, to provide access to meals designed to support the treatment of chronic diseases. As part of the Vintage FPCI Altaroc Odyssey portfolio, CookUnity is putting its culinary model to work for public health.

Article

|

18

A must

North America

Consumption

No items found.

Odyssey 2021

CookUnity

CookUnity

Follow portfolio news

GCash becomes compatible with Google Pay for 75 million Filipinos

GCash, featured in the Vintage FPCI Altaroc Odyssey , has taken another step forward by becoming compatible with Google Pay, paving the way for faster and more secure payments for 75 million Filipinos. This integration, which is being rolled out gradually on a large scale, will allow everyone to link their GCash wallet to Google Pay for easy payments.

Article

|

18

Innovative

Rest of the world

Consumption

No items found.

Odyssey 2021

GCash

GCash

Follow portfolio news

ScreenPoint Medical facilitates breast cancer diagnosis in Washington State

ScreenPoint Medical, a company included in the Vintage FPCI Altaroc Odyssey portfolio, is taking its AI technology to the next level with its launch at RAYUS Radiology centers in Washington State. Already used for more than ten million mammograms worldwide, the Dutch company’s AI provides radiologists with an additional perspective to detect certain signs of breast cancer earlier.

Article

|

18

Positive impact

North America

Healthcare

No items found.

Odyssey 2021

ScreenPoint

ScreenPoint

Follow portfolio news

VAST Data partners with Microsoft to simplify AI usage

VAST Data has just announced a partnership with Microsoft that will soon allow Azure users (Microsoft’s cloud ecosystem) to access the VAST AI OS. This new platform [DH1.1] has been designed to meet the needs of the most advanced artificial intelligence. A portfolio company in the Vintage FPCI Altaroc Odyssey fund, VAST Data is one of the global leaders in data storage for artificial intelligence.

Article

|

18

Unicorn

North America

Technology / Software

No items found.

Odyssey 2021

Vast Data

Vast Data

Follow portfolio news

CompanyCam now valued at $2 billion

CompanyCam has just been valued at $2 billion following a record-breaking $415 million funding round, making it the first-ever unicorn to be founded and developed in Nebraska. Part of the Vintage FPCI Altaroc Odyssey portfolio, CompanyCam offers a platform designed to document construction sites through the cloud-based sharing of photos and videos.

Article

|

05

Strong growth

North America

Technology / Software

No items found.

Odyssey 2021

CompanyCam

CompanyCam

Follow portfolio news

Cybersecurity: Brinqa doubles its sales in the third quarter

Based in Texas, Brinqa posted strong results for the third quarter of 2025, driven by the launch of BrinqaIQ, which enables IT teams to get an immediate, clear answer regarding IT security. Brinqa, which is part of the Vintage FPCI Altaroc Odyssey portfolio, is already making waves with its cybersecurity risk management platform, which has been adopted by Nestlé, among others.

Article

|

05

Innovative

North America

Technology / Software

No items found.

Odyssey 2021

Brinqa

Brinqa

Follow portfolio news

Insurance broker GGW signs its second acquisition of the year in Spain

The German insurance brokerage group GGW, which is part of the Vintage FPCI Altaroc Odyssey fund, has just acquired Costa Serra, a Catalan brokerage firm founded in 1989. This transaction marks GGW’s second expansion into Spain this year and underscores its ambition to rapidly strengthen its presence there.

Article

|

05

A must

Europe

Consumption

No items found.

Odyssey 2022

GGW

GGW

Follow portfolio news

VAST Data receives $1.17 billion to become the central database for Open AI and Meta's AI systems

VAST Data has signed a $1.17 billion commercial agreement with CoreWeave, one of the most innovative players in the AI cloud sector, which already serves clients such as OpenAI and Meta. Based in New York and part of the Vintage FPCI Altaroc Odyssey portfolio, VAST Data is a global leader in data storage, working with renowned institutions such as Pixar and the University of California, Berkeley.

Article

|

05

Unicorn

North America

Technology / Software

No items found.

Odyssey 2021

Vast Data

Vast Data

Understanding Private Equity

Private Equity: A Guide for Investors

Private equity funds invest in privately held companies.

In this video, you’ll explore the entire investment cycle: key players, strategies, value creation, and exits.

Video

|

27

No items found.

No items found.

Understanding Current Trends in Private Equity & Introduction to Vintage Odyssey Vintage

Learn about our assessment of the current market environment and the investment convictions that underpin the construction of Vintage Odyssey . This new portfolio is part of a rigorous and selective investment strategy designed to capitalize on opportunities in the current market cycle.

Video

|

15

Odyssey 2025

No items found.

Hg

K1 Management

Insight Partners

Nordic Capital

New Mountain Capital

Discover Altaroc

Launch Webinar for the 5th Vintage Altaroc Odyssey

Discover the Vintage Altaroc Odyssey our investment approach, which combines institutional expertise, technology, and innovation. This session explores the fundamentals of the Altaroc strategy, the drivers of value creation, and the tailored solutions we offer to address your clients’ specific challenges.

Video

|

03

Odyssey 2025

Odyssey 2025

Hg

K1 Management

Insight Partners

Nordic Capital

New Mountain Capital

Discover Altaroc

Building a solid long-term wealth management strategy

In a challenging environment, clients are looking for solutions tailored to their long-term financial goals. Re-Up addresses this need by offering a structured and sustainable approach.

Video

|

11

Odyssey 2025

Odyssey 2025

Nordic Capital

New Mountain Capital

K1 Management

Hg

Insight Partners

Odyssey : Presentation of the first funds raised and discussions with three industry experts

Watch the recording of the webinar on the Altaroc Odyssey cohort.

On the agenda: a presentation of the first selected funds, an analysis of market dynamics, and discussions with private equity experts.

Clear insights to help you understandAltaroc investment strategyAltaroc the outlook for the 2024 cohort.

Video

|

12

Odyssey 2024

Odyssey 2024

Bridgepoint

Vitruvian

Thoma Bravo

Summit Partners

Discover Altaroc

Private equity's strengths in a global economy

Webinar presenting the Odyssey funds, private equity opportunities, and the key advantages of this asset class in the current global economic climate.

Video

|

23

Odyssey 2024

Odyssey 2024

Bridgepoint

Vitruvian

Thoma Bravo

Summit Partners

Discover Altaroc

Launch Webinar for the 3rd Vintage Altaroc Odyssey

Relive the launch event for the 3rd Vintage Altaroc Odyssey an overview of the portfolio, investment strategy, and related outlook.

Video

|

06

Odyssey 2023

Odyssey 2023

New Mountain Capital

Inflexion

Main Capital

TA Associates

CVC

Mastering the challenges of private equity

Interview - Chris Busby - Managing Partner - Bridgepoint

In an increasingly complex market, Bridgepoint on the mid-market and discipline.

Video

|

14

No items found.

Bridgepoint

Mastering the challenges of private equity

Interview with Scott Crabill - Managing Partner - Thoma Bravo

AI and Software: Thoma Bravo’s Strategy to Transform Private Equity

Video

|

14

No items found.

Thoma Bravo

.webp)

Follow portfolio news

Interview with Ian Drysdale, CEO of One Inc.

Learn about the career of Ian Drysdale, CEO of One Inc, a specialist in payment infrastructure for the insurance industry.

Video

|

09

Odyssey 2021

No items found.

Nordic Capital

Mastering the challenges of private equity

Interview with Briac Houtteville, Managing Director - Future Standard

The role of Evergreen and secondary education: interview with Briac Houtteville.

Video

|

13

Altalife 2023

Altaroc Global Evergreen

Discovery FCPR

Horizon 2024

Horizon 2025

No items found.

Mastering the challenges of private equity

Interview with Paul Fishbin, Managing Director - Manulife

Paul Fishbin explains how Manulife built a long-term private equity program.

Video

|

09

Altalife 2023

Altaroc Global Evergreen

Discovery FCPR

Horizon 2024

Horizon 2025

No items found.

Follow portfolio news

Interview with Daniel Baker, CEO of Healthdrive

In Boston, Daniel Baker, CEO of HealthDrive, shares his vision for sustainable growth with a human impact.

Video

|

29

Altalife 2023

Altaroc Global Evergreen

Discovery FCPR

Horizon 2024

Horizon 2025

No items found.

Deciphering trends

Inside Private Equity - Broadcast on December 17, 2025

Inside Private Equity with François Georges, Dominica Adam, and Maurice Tchenio, among others

Video

|

17

Odyssey 2021

Odyssey 2022

Odyssey 2023

Odyssey 2024

Odyssey 2025

Seven2

Mastering the challenges of private equity

Interview with David Rogero - Partner at Cressey & Company

Discover episode 2 of Fund Insights with David Rogero, dedicated to Cressey & Company healthcare strategy.

Video

|

08

Odyssey 2021

Altalife 2023

Altaroc Global Evergreen

Discovery FCPR

Horizon 2024

Cressey & Company

Follow portfolio news

Interview Jeff Wessler - CEO Heartbeat

Dr. Jeff Wessler, founder of Heartbeat Health, pioneer of virtual-first cardiology in the United States

Video

|

25

Odyssey 2022

Odyssey 2022

Horizon 2025

Cressey & Company

Deciphering trends

Inside Private Equity - November 26, 2025 issue

Inside Private Equity with Olivier Farouz, Briac Houtteville, and Frédéric Stolar, among others

Video

|

29

Odyssey 2021

Odyssey 2022

Odyssey 2023

Odyssey 2024

Odyssey 2025

No items found.

Deciphering trends

Inside Private Equity - October 15, 2025 issue

Inside Private Equity with Thomas Vandeville, Chris Bon, and Louis Flamand, among others.

Video

|

16

Odyssey 2021

Odyssey 2022

Odyssey 2023

Odyssey 2024

Odyssey 2025

No items found.

Mastering the challenges of private equity

Interview Peter Y. Chung - Summit Partners

Interview with Peter Y. Chung, Managing Director and CEO of Summit Partners recorded in Boston on October 28, 2024.

Video

|

03

Odyssey 2024

Horizon 2024

Summit Partners

Mastering the challenges of private equity

Interview Steve Klinsky - New Mountain Capital

Interview with Steve Klinsky, Founder and CEO of New Mountain Capital

Video

|

24

Odyssey 2023

Odyssey 2023

Horizon 2025

Odyssey 2025

New Mountain Capital

Mastering the challenges of private equity

Interview Stephen Byrne - Vitruvian

Interview with Stephen Byrne, Partner at Vitruvian Partners

Video

|

10

Odyssey 2024

Odyssey 2024

Horizon 2024

Vitruvian

Deciphering trends

Inside Private Equity - Issue of September 24, 2025

Inside Private Equity with Pascal Girin, Olivier de Vilmorin, and Frédéric Stolar.

Video

|

25

Odyssey 2021

Odyssey 2022

Odyssey 2023

Odyssey 2024

Odyssey 2025

No items found.

Deciphering trends

Inside Private Equity - July 9, 2025 issue

Inside Private Equity with Jean-Michel Breul, Edouard Didier, and Louis Flamand

Video

|

08

Odyssey 2021

Odyssey 2022

Odyssey 2023

Odyssey 2024

Odyssey 2025

No items found.

Deciphering trends

Inside Private Equity - June 25, 2025 issue

Inside Private Equity special featuring Maurice Tchenio with Alain Afflelou and Jean-Sébastien Decaux

Video

|

25

Odyssey 2021

Odyssey 2022

Odyssey 2023

Odyssey 2024

Odyssey 2025

No items found.

Deciphering trends

Inside Private Equity - June 4, 2025 issue

Inside Private Equity with Maxime Dubois, Julien Krantz, and Louis Flamand.

Video

|

05

Odyssey 2021

Odyssey 2022

Odyssey 2023

Odyssey 2024

Odyssey 2025

No items found.

Deciphering trends

Inside Private Equity - Issue of April 23, 2025

Inside Private Equity with Samuel Hassine, Jean-Christel Trabarel, and Frédéric Stolar.

Video

|

23

Odyssey 2021

Odyssey 2022

Odyssey 2023

Odyssey 2024

Odyssey 2025

No items found.

Mastering the challenges of private equity

Interview Darren Foreman - PSERS

Darren Foreman details the allocation of pension funds to private equity.

Video

|

03

Odyssey 2021

Odyssey 2022

Odyssey 2023

Odyssey 2024

Odyssey 2025

No items found.

Mastering the challenges of private equity

Interview Jean-Baptiste Brian - Partner Hg

Why the software sector has become central, and how a specialist investor creates value.

Video

|

03

Odyssey 2022

Odyssey 2025

Altalife 2023

Hg

Follow portfolio news

Interview Anish Thakkar - Co-founder Sun King

Interview with Sun King's co-founder on growth and impact in private equity.

Video

|

18

Odyssey 2021

Odyssey 2021

No items found.

Follow portfolio news

Interview Merete Hverven - CEO Visma

From Oslo, Merete Hverven presents Visma's trajectory, supported by private equity.

Video

|

27

Odyssey 2023

Altalife 2023

Hg

Deciphering trends

Inside Private Equity - Issue of March 26, 2025

Inside Private Equity with Manuel Liedot, John Hazan, and Julie Van Campenhoudt.

Video

|

26

Odyssey 2024

Odyssey 2024

No items found.

.jpeg)

Understanding Private Equity

The software sector in Private Equity

Analysis of the role of software publishers in private equity strategies.

Video

|

03

Odyssey 2025

Odyssey 2025

Horizon 2025

No items found.

.jpeg)

Discover Altaroc

Introduction to Fund manager Hg

Hg, a leading player in LBO in Europe and a long-standing partner ofAltaroc.

Video

|

03

Odyssey 2025

Odyssey 2025

Hg

.jpeg)

Discover Altaroc

Introduction to the Fund manager Insight Partners

Insight Partners, a software specialist, supports hypergrowth internationally.

Video

|

03

Odyssey 2025

Odyssey 2025

Insight Partners

.jpeg)

Discover Altaroc

Introducing the Vintage Altaroc Odyssey FPCI

Launch ofOdyssey with increased allocation to technology and software.

Video

|

03

Odyssey 2025

Odyssey 2025

No items found.

.jpeg)

Discover Altaroc

The selection universe of the Altaroc Odyssey 2025 Vintage

Odyssey brings together seven funds targeting software, healthcare, and services in Europe and the United States.

Video

|

03

Odyssey 2025

Odyssey 2025

No items found.

Mastering the challenges of private equity

Interview with Saniya Jamil, Senior Director at Thoma Bravo (extract from BFM Business, 30/10)

Sania Jamil presents Thoma Bravo's B2B software strategy and growth drivers.

Video

|

20

Odyssey 2024

Odyssey 2024

Thoma Bravo

Mastering the challenges of private equity

Interview with Orlando Bravo, Founder and Managing Partner - Thoma Bravo

Interview with Orlando Bravo, founder of Thoma Bravo and Fund manager Odyssey .

Video

|

13

Odyssey 2024

Odyssey 2024

Horizon 2024

Thoma Bravo

Deciphering trends

Inside Private Equity - Issue of February 26, 2025

Inside Private Equity with Aleksandra Putra, Emmanuel Olivier, and Louis Flamand.

Video

|

26

Odyssey 2024

Odyssey 2024

No items found.

Follow portfolio news

Interview with Mike Capone, CEO of Qlik

Mike Capone explains the role of private equity in Qlik's SaaS transformation.

Video

|

06

Odyssey 2024

Odyssey 2024

No items found.

Follow portfolio news

Interview Jean-Matthieu Biseau - Opteven

Jean-Mathieu Biseau shares his experience of growth through four LBO .

Video

|

27

Odyssey 2021

Odyssey 2021

No items found.

Mastering the challenges of private equity

Interview Xavier Robert Chief Investment Officer - Bridgepoint

Xavier Robert analyzes the macroeconomic environment and Bridgepoint strategy.

Video

|

20

Odyssey 2024

Odyssey 2022

Odyssey 2024

Bridgepoint

Discover Altaroc

Altaroc Partners, a pioneering private equity management company

In four years, 6,000 investors have chosen Altaroc invest in private equity.

Video

|

23

Odyssey 2024

Odyssey 2024

No items found.

Understanding Private Equity

Liquidity in Private Equity

Dimitri Bernard explains performance and liquidity management in private equity.

Video

|

23

Odyssey 2024

Odyssey 2024

No items found.

.jpeg)

Discover Altaroc

Vintage Altaroc Odyssey co-investment performance

Claire Peyssard presents the performance ofAltaroc recent co-investments.

Video

|

23

Odyssey 2024

Odyssey 2024

No items found.

.jpeg)

Follow portfolio news

Entrepreneur interviews

Jean-Mathieu Biseau and Mike Capone attest to growth sustained by private equity.

Video

|

23

Odyssey 2024

Odyssey 2024

No items found.

.jpeg)

Deciphering trends

Interview with Xavier Robert, Chief Investment Officer of Brigepoint, on the macro-economic context and its impact on private equity.

Xavier Robert analyzes the macroeconomic impact on private equity.

Video

|

23

Odyssey 2024

Odyssey 2022

Odyssey 2024

Bridgepoint

Understanding Private Equity

Why market timing makes no sense in private equity

Private equity favors a long-term horizon and gradual deployment.

Video

|

02

Odyssey 2021

Odyssey 2022

Odyssey 2023

Odyssey 2024

Odyssey 2025

No items found.

Understanding Private Equity

Private equity performance drivers

Private equity offers performance, diversification, and access to a broader universe.

Video

|

02

Odyssey 2021

Odyssey 2022

Odyssey 2023

Odyssey 2024

Odyssey 2025

No items found.

Understanding Private Equity

Understanding private equity fees

Why private equity fees contribute to net performance.

Video

|

02

Odyssey 2021

Odyssey 2022

Odyssey 2023

Odyssey 2024

Odyssey 2025

No items found.

Discover Altaroc

Revolutionizing the approach

Structure your private equity allocation withAltaroc Re-Up strategy.

Video

|

02

Odyssey 2021

Odyssey 2022

Odyssey 2023

Odyssey 2024

Odyssey 2025

No items found.

Understanding Private Equity

Why waiting is not a winning strategy

Invest in private equity without delay thanks to a vintage approach.

Video

|

02

Odyssey 2021

Odyssey 2022

Odyssey 2023

Odyssey 2024

Odyssey 2025

No items found.

Understanding Private Equity

Generalist vs. specialist funds

Generalist or specialist funds: what are the differences in private equity?

Video

|

12

Odyssey 2021

Odyssey 2022

Odyssey 2023

Odyssey 2024

Odyssey 2025

No items found.

Deciphering trends

Inside Private Equity - Issue of January 29, 2025

Inside Private Equity with Romain Peninque, Maurice Tchenio, and Guillaume Lorain.

Video

|

30

Odyssey 2024

Odyssey 2024

No items found.

Deciphering trends

Isabelle Pagnotta, Partner at Inflexion in the Inside Private Equity program on BFM Business

Isabelle Pagnotta discusses trends in private equity on BFM Business.

Video

|

22

Odyssey 2023

Inflexion

Mastering the challenges of private equity

Interview John Hartz, Co-founder and Managing Partner - Inflexion

Interview with John Hartz on minority investment in private equity.

Video

|

15

Odyssey 2023

Inflexion

Discover Altaroc

A newsflow for real-time portfolio updates

A news feed to follow portfolio news in real time.

Video

|

05

No items found.

No items found.

Discover Altaroc

An Investors Platform track the performance of Vintage funds

An Investors Platform to tracking Vintage.

Video

|

05

No items found.

No items found.

Discover Altaroc

A Partners Platform as a one-stop-shop

A Partners Platform as a dedicated one-stop-shop.

Video

|

05

No items found.

No items found.

Discover Altaroc

A holistic website

A website designed as a holistic platform.

Video

|

05

No items found.

No items found.

Deciphering trends

Inside Private Equity - The Big Debrief, 18 December 2024

Inside Private Equity with Clément Delpirou, Bertrand Pivin, and Frédéric Stolar.

Video

|

18

Odyssey 2024

Odyssey 2024

No items found.

Deciphering trends

Inside Private Equity - 18 December 2024 broadcast

Inside Private Equity's Grand Debrief with Clément Delpirou, Bertrand Pivin, and Louis Flamand.

Video

|

18

Odyssey 2024

Odyssey 2024

Seven2

Discover Altaroc

Review of the BFM Business partnership and Altaroc’s support strategy

A look back at the partnership with BFM Business andAltaroc supportAltaroc private equity.

Video

|

12

Odyssey 2024

Odyssey 2024

No items found.

Discover Altaroc

Presentation of the first Odyssey 2024 Vintage companies

Discover the companies of the Odyssey vintage and their potential in private equity.

Video

|

12

Odyssey 2024

Odyssey 2024

No items found.

Discover Altaroc

Introducing the first managers of Millésime Odyssey 2024